When you push that enter key, your stock order is sent over the internet to your broker. Your broker then decides which market to send it to for execution. Understanding this process matters because where and how your order is executed can impact the price you pay and the overall cost of your transaction.

Many investors never think about what happens between clicking “buy” and seeing shares appear in their account. But behind every trade is a complex system of routing decisions, regulatory obligations, and clearing processes. Our team spent weeks analyzing execution quality reports and speaking with industry professionals to bring you this complete breakdown of how online brokers execute trades.

In this guide, you will learn the exact path your order takes, the venues where trades are executed, and how regulations protect your interests. We will also explain fractional share mechanics that no other guide covers and show you how to verify your broker is giving you fair execution.

Table of Contents

Key Takeaways

- Your order travels through a 5-step process from placement to settlement

- Brokers route orders to exchanges, market makers, or ECNs based on best execution obligations

- Payment for order flow creates potential conflicts of interest you should understand

- T+1 settlement means trades complete one business day after execution

- Your broker must provide 606 reports showing where your orders were routed

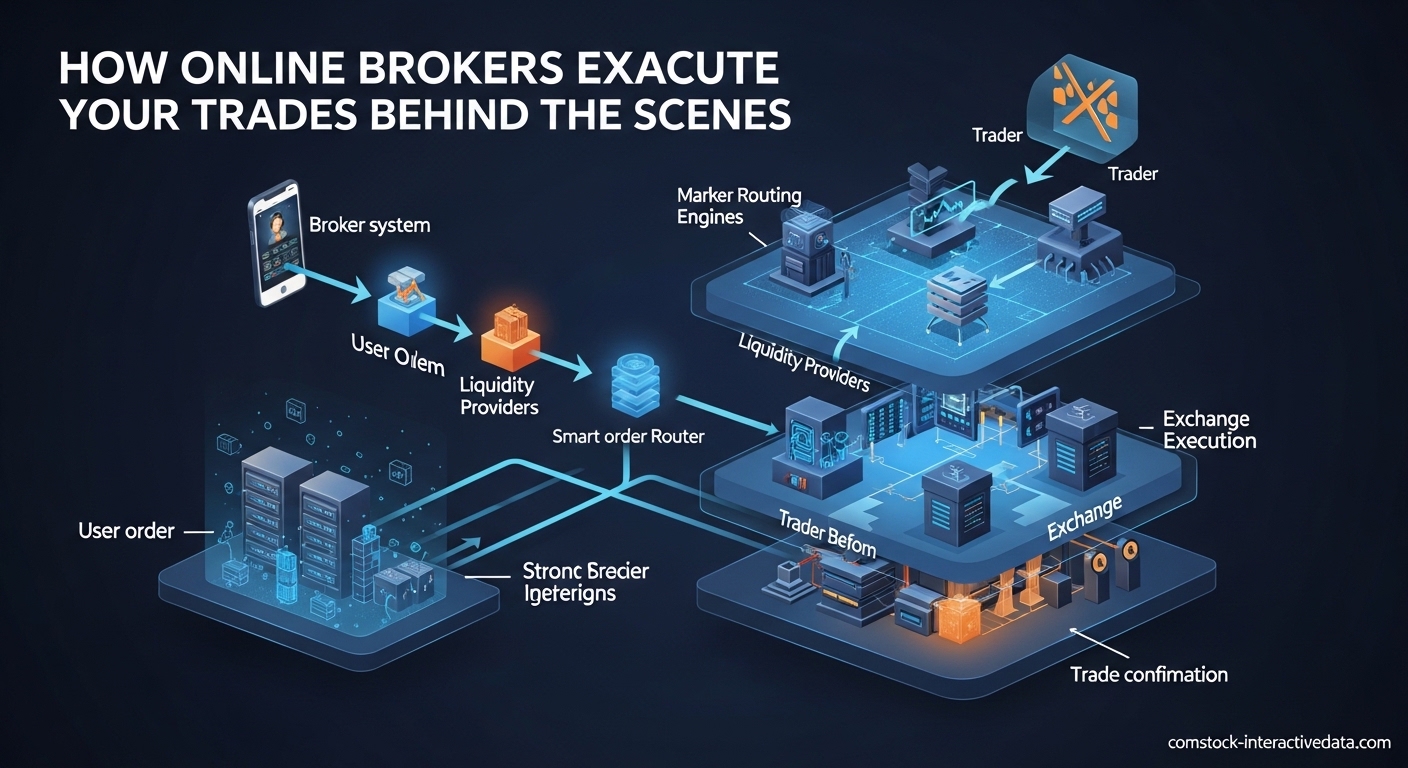

How Online Brokers Execute Trades: The 5-Step Process

The trade lifecycle follows a predictable sequence from the moment you click submit. Each step involves different systems, regulatory checks, and market participants. Here is exactly what happens when you place a stock order in 2026.

Step 1: You Place Your Order

You open your broker’s mobile app or desktop platform and enter your trade details. You select the ticker symbol, quantity, and order type. Market orders execute immediately at the best available price, while limit orders only execute at your specified price or better.

Your broker’s system immediately performs a suitability screening. This compliance check verifies you have sufficient buying power for purchases or sufficient holdings for sales. The system also checks for pattern day trading restrictions if you are trading on margin.

Step 2: Your Order Reaches the Broker’s Order Management System

Once validated, your order enters the broker’s order management system. This software routes orders to various execution venues based on complex algorithms. Modern systems process this routing decision in milliseconds.

Your broker now faces a critical decision. They must choose where to send your order for execution. This decision is governed by their legal obligation to seek best execution for your trade.

Step 3: The Broker Routes Your Order to an Execution Venue

Your broker evaluates multiple venues to find the best place for your order. They might send it to a major exchange like NYSE or Nasdaq. Alternatively, they could route to a market maker, an electronic communications network (ECN), or even fill it internally from their own inventory.

The routing decision considers price, speed, and likelihood of execution. Your broker’s order routing system continuously monitors quotes across all available venues. This happens in a fraction of a second.

Step 4: Your Trade Is Executed and Matched

At the execution venue, your buy order is matched with a sell order from another party. Market makers facilitate this matching by providing liquidity and quoting bid-ask spreads. Once matched, the trade is time-stamped and recorded.

You receive an electronic confirmation within seconds. This confirmation shows the execution price, quantity filled, and time of execution. Your broker’s system updates your account to reflect the new position immediately.

Step 5: Clearing and Settlement

Execution is only part of the story. The trade must now clear and settle through the Depository Trust and Clearing Corporation (DTCC). In 2026, trades settle on T+1, meaning one business day after execution. This replaced the previous T+2 standard in May 2024.

During settlement, ownership officially transfers from seller to buyer. Cash moves from buyer to seller. The shares appear in your account as “settled” once this process completes.

Where Your Order Goes: Exchanges, Market Makers, and ECNs

Your broker has several options when deciding where to execute your trade. Each venue type operates differently and offers distinct advantages. Understanding these differences helps you make informed decisions about order placement.

Major Stock Exchanges

The New York Stock Exchange and Nasdaq remain the most visible execution venues. These exchanges use auction markets where buyers and sellers submit orders that are matched electronically. Designated market makers at the NYSE and Nasdaq market makers help ensure orderly trading.

Exchanges offer transparency and competitive pricing through visible order books. Your broker can route directly to these exchanges or access them through other means. Exchange execution typically provides immediate price discovery.

Market Makers and Wholesale Broker-Dealers

Market makers maintain inventories of stocks and quote bid-ask spreads continuously. They profit from the spread while providing liquidity to the market. When your broker routes to a market maker, that firm may execute against its own inventory or route further.

Many retail brokers route orders to wholesale broker-dealers like Citadel Securities or Virtu Financial. These firms pay brokers for order flow, which creates revenue for commission-free brokers. This practice, called payment for order flow, has drawn regulatory scrutiny.

Electronic Communications Networks (ECNs)

ECNs are computerized systems that match orders automatically without traditional market makers. They connect buyers and sellers directly and often offer access to pre-market and after-hours trading. Popular ECNs include venues operated by major exchanges and independent networks.

Institutional traders frequently use ECNs for large block trades that might move prices on public exchanges. These networks provide anonymity and can reduce market impact for substantial orders.

Dark Pools and Alternative Trading Systems

Dark pools are private exchanges where institutional investors trade large blocks without revealing their intentions to the public market. Your broker may route some orders to these alternative trading systems (ATSs) if they believe it serves your interest.

Dark pool execution represents about 40% of total US equity volume according to industry data. While they offer reduced market impact, they also operate with less transparency than public exchanges.

Best Execution: Your Broker’s Legal Obligation

When your broker routes your order, they are bound by a regulatory obligation to seek best execution. FINRA Rule 5310 and SEC Regulation NMS establish this standard. But what does “best execution” actually mean for your trades?

Understanding the Best Execution Standard

Best execution does not mean your broker must find the absolute lowest price for every buy order. Instead, brokers must consider the full range of factors including price, speed, likelihood of execution, and order size. The goal is the most favorable terms reasonably available under the circumstances.

Brokers must regularly review their order routing practices. They must analyze execution quality across different venues and adjust routing decisions accordingly. This ongoing duty ensures they are not simply routing to the venue that pays them the most.

Payment for Order Flow Explained

Many commission-free brokers generate revenue through payment for order flow. Market makers pay brokers for the right to execute their customers’ retail orders. This practice can create apparent conflicts of interest between broker profit and customer execution quality.

Brokers must disclose their payment for order flow arrangements. You can find this information in your account agreement and on their website. SEC Rule 606 requires brokers to publish quarterly reports showing where they routed orders and what payments they received.

Internalization: When Brokers Fill From Their Own Inventory

Some brokers act as market makers for their own customers’ orders. When you place an order, your broker might fill it internally from their own inventory rather than routing to an external venue. This practice, called internalization, can provide faster execution.

Internalized trades must still meet best execution standards. Your broker must verify they are giving you a price at least as good as what was available at external venues. This is known as the “protected quote” requirement under Regulation NMS.

Price Improvement and Execution Quality

Many brokers now tout price improvement statistics. Price improvement occurs when your order executes at a better price than the quoted national best bid or offer (NBBO). For example, you might place a market order when the ask is $50.25 and receive execution at $50.23.

Market makers can offer price improvement because they see the full flow of retail orders. They use this information to refine their pricing and often share some benefit with the retail trader. Your broker should report how frequently you receive price improvement.

Understanding Clearing and Settlement: T+1 Explained

Execution is only half the story. After your trade matches, it enters the clearing and settlement process. This backend machinery ensures ownership transfers properly and money changes hands securely.

The Difference Between Executing and Clearing Brokers

Executing brokers process your buy and sell orders. They handle the front-end decisions about where to route and how to fill your trades. Many retail brokers you recognize by name primarily function as executing brokers.

Clearing brokers handle the back-office functions. They ensure trades settle properly, maintain custody of securities, and handle regulatory reporting. Some firms perform both functions while others use separate clearing firms.

The Role of the DTCC and Clearinghouses

The Depository Trust and Clearing Corporation sits at the center of US securities settlement. This entity maintains records of who owns what and facilitates the transfer of securities between parties. When you buy a stock, the DTCC system updates to reflect your ownership.

Clearinghouses also manage risk by requiring margin deposits from brokers. They guarantee trade completion even if one party fails. This system has prevented market disruptions for decades.

T+1 Settlement: What Changed in 2024

The US securities markets moved to T+1 settlement in May 2024. Under this standard, trades settle one business day after execution. If you buy stock on Monday, settlement occurs on Tuesday.

This change from the previous T+2 standard reduces counterparty risk and frees up capital in the financial system. However, it also means you must have funds available sooner to pay for purchases. Free riding violations can occur if you sell shares before paying for them.

SIPC Protection for Your Account

Many investors worry about the safety of assets held at brokerage firms. The Securities Investor Protection Corporation (SIPC) provides insurance coverage for securities and cash held by broker-dealers. SIPC protects up to $500,000 per customer, including a $250,000 limit for cash claims.

This protection covers firm failures, not market losses. If your broker goes bankrupt, SIPC works to return your securities. Many brokers also purchase additional private insurance beyond SIPC limits.

How Fractional Shares Are Executed?

Fractional share trading has become increasingly popular with retail investors. But how do brokers actually execute an order for 0.5 shares of Amazon or 0.1 shares of Berkshire Hathaway? This process differs significantly from whole-share execution.

The Mechanics of Fractional Share Matching

When you place a fractional order, your broker pools your request with orders from other customers. If five customers each want 0.2 shares of a stock, the broker combines them into a single whole-share order. This combined order then executes through normal market channels.

After the bulk order fills, your broker allocates fractional portions to individual accounts. This allocation happens internally based on the price of the combined execution. You receive ownership of a fractional interest in the broker’s inventory.

Order Types and Fractional Execution

Most brokers only support market orders for fractional shares. Limit orders are typically unavailable because the pooling process requires aggregation before routing. This limitation means you have less price control with fractional trades.

Some brokers maintain their own inventory of popular stocks for fractional execution. They may fill your order internally from existing fractional positions held by other customers who recently sold. This internal matching happens instantly.

Dividend Reinvestment and Fractional Shares

Dividend reinvestment plans (DRIPs) often generate fractional shares automatically. When your dividend payment is insufficient to purchase a whole share, the broker executes a fractional purchase on your behalf. This process follows the same pooling mechanics as intentional fractional orders.

How to Check Your Trade Execution Quality?

Brokers are required to provide transparency about their order routing and execution practices. You can use this information to evaluate whether your broker is serving your interests. Here is how to access and interpret these reports.

Understanding 606 Reports

SEC Rule 606 requires brokers to publish quarterly reports detailing their order routing. These reports show what percentage of orders went to each venue and whether the broker received payment for order flow. You can typically find these reports in the “About Us” or “Legal” sections of your broker’s website.

When reviewing 606 reports, look for concentration at a single venue. If 90% of your non-directed orders go to one market maker, your broker may be prioritizing payment over execution quality. Diverse routing suggests the broker is actively seeking best execution.

Price Improvement Data

Many brokers now publish statistics on price improvement. These reports show how often customers receive better prices than the NBBO at order entry. Compare your broker’s price improvement rate to industry averages published by regulators.

Keep in mind that price improvement is only one factor. A broker with high price improvement but slow execution may not serve active traders well. Consider your trading style when evaluating these statistics.

Red Flags to Watch For

Certain practices may indicate your broker is not prioritizing your execution quality. Be concerned if your market orders consistently execute at worse prices than the quoted spread. Watch for significant delays in order confirmation during normal market conditions.

Brokers who refuse to provide execution quality reports or make them difficult to find deserve scrutiny. Transparency is a hallmark of reputable firms. Commission-free trading is not free if poor execution costs you more than commissions would have.

Frequently Asked Questions

How do brokers execute trades?

Brokers execute trades by routing your order to execution venues such as stock exchanges, market makers, or electronic communications networks (ECNs). They use order management systems to evaluate options and select the venue offering the best combination of price, speed, and likelihood of execution. Once matched at the venue, the trade is confirmed and sent for clearing and settlement.

What is order execution in trading?

Order execution is the process by which your buy or sell order is routed from your online broker to the appropriate market venue where it is matched with a counterparty and completed. Execution includes the routing decision, matching at the venue, confirmation to the customer, and the subsequent clearing and settlement process.

Is it safe to have more than $500,000 in a brokerage account?

Yes, it is generally safe to hold more than $500,000 at a reputable brokerage firm. SIPC insurance covers up to $500,000 per customer, but many brokers carry additional private insurance that extends protection into the millions. However, SIPC does not protect against market losses, only against firm failure. Consider spreading large balances across multiple firms if you are concerned.

Why do some trades execute faster than others?

Execution speed varies based on order type, market conditions, and routing destination. Market orders typically execute faster than limit orders because they accept any available price. Orders routed to market makers or internalized by your broker often execute faster than those sent to exchanges. During high volatility periods, execution may slow due to increased order volume and price fluctuations.

What prevents a trade from executing?

Several factors can prevent execution including insufficient liquidity at your limit price, trading halts on the security, circuit breakers during market volatility, or insufficient buying power in your account. Limit orders only execute if the market reaches your specified price. Orders placed outside regular trading hours may not execute until the market opens unless routed to after-hours venues.

Conclusion

Understanding how online brokers execute trades empowers you to make better decisions about where and how you invest. The journey from click to settlement involves complex systems working together in milliseconds. Your broker’s routing choices, the venues they select, and the regulatory framework all impact your trading experience.

Remember that best execution is your legal right as an investor. Review your broker’s 606 reports periodically. Watch for price improvement on your trades. Ask questions if execution seems consistently poor. The mechanics behind your trades should work for you, not against you.

Whether you are placing your first trade or your thousandth, knowing what happens behind the scenes helps you trade with confidence. The markets have never been more accessible. Understanding how they work ensures you get the most from that access.