Every time you see a stock price flicker on your screen, something extraordinary happens behind the scenes. Billions of market data messages race through a complex infrastructure, traveling from stock exchanges to your trading app in mere microseconds. The system that makes this possible is called a ticker plant.

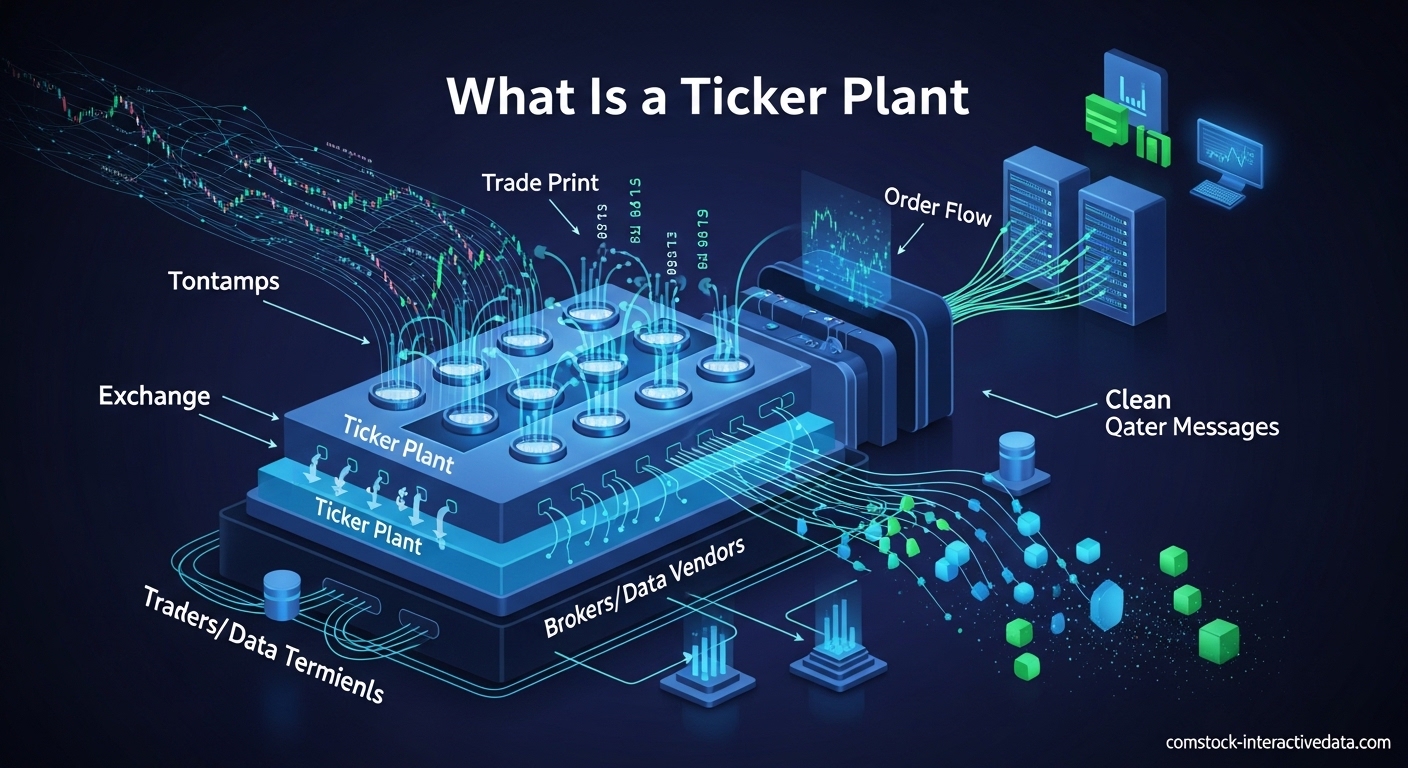

A ticker plant is a specialized system that aggregates market data from multiple exchanges, normalizes it into a standard format, and distributes it to trading applications in real-time. Think of it as the central nervous system of financial markets, receiving raw data from dozens of sources and delivering clean, consistent information to thousands of destinations.

In this guide, we will explore what a ticker plant is, how it processes market data, and why these systems have become the backbone of modern electronic trading. Whether you are a financial professional or simply curious about market infrastructure, you will gain a clear understanding of how market data flows from exchanges to your screen.

Table of Contents

What Is a Ticker Plant?

A ticker plant is essentially a high-performance data processing hub that sits between financial exchanges and the applications that consume market data. It receives raw feeds from stock exchanges, futures markets, options venues, and other trading platforms. Then it transforms that data into a uniform format that downstream systems can understand and use.

The term “ticker plant” traces its roots to the ticker tape era of the late 1800s. Back then, stock prices were printed on narrow strips of paper by telegraph-based ticker machines. The “plant” referred to the room full of these machines and the operators who managed them. Today, the name persists even though the technology has evolved from mechanical printers to sophisticated software and hardware systems.

The Core Functions of a Ticker Plant

Modern ticker plants perform three essential functions that keep financial markets running smoothly. First, they ingest data from multiple sources simultaneously. Each exchange sends data in its own proprietary format and protocol. The ticker plant must handle these diverse streams without dropping messages, even during market surges.

Second, ticker plants normalize data into a consistent format. They strip away exchange-specific encoding and convert everything into a standardized structure. This normalization allows trading applications to work with any exchange feed without needing custom parsers for each source.

Third, they distribute the processed data to downstream consumers. These might include trading algorithms, risk management systems, charting applications, or retail brokerage platforms. The ticker plant acts like a sophisticated traffic cop, ensuring each subscriber receives exactly the data they need at the speed they require.

Why the “Traffic Cop” Analogy Works?

One helpful way to understand a ticker plant is to picture a busy intersection with a traffic officer directing cars. Data flows in from multiple directions (exchanges), gets organized and prioritized, then flows out to various destinations (trading applications). Without this coordination, the system would descend into chaos.

Just as a traffic cop prevents accidents and keeps vehicles moving efficiently, a ticker plant prevents data bottlenecks and ensures every message reaches its destination. The analogy breaks down only in scale. While a traffic cop might handle hundreds of cars per hour, a modern ticker plant processes billions of messages daily.

How Does a Ticker Plant Process Market Data?

Market data processing happens in distinct stages, each optimized for speed and accuracy. The entire pipeline from exchange to end-user typically completes in under 100 microseconds, with the fastest systems achieving latencies of just a few microseconds. Understanding each stage helps explain why this infrastructure matters so much to modern trading.

Step 1: Data Ingestion from Multiple Exchanges

The journey begins at the exchange level. Stock exchanges like the NYSE, NASDAQ, and CBOE generate massive streams of market data. Every trade execution, every order modification, and every price update gets packaged into messages and sent out through dedicated network feeds. A single busy exchange might generate over 10 million messages per second during peak trading.

Ticker plants connect to these exchanges through dedicated network links. Many firms use colocation services, placing their ticker plant hardware in the same data center as the exchange servers. This physical proximity reduces network latency to mere microseconds. Some ultra-low-latency setups achieve round-trip times of less than one microsecond between exchange and ticker plant.

Modern ticker plants ingest data from dozens of sources simultaneously. They might handle equities from multiple exchanges, options data from OPRA, futures from CME, and forex from various global venues. Each source uses different protocols, message formats, and network configurations. The ingestion layer must handle this diversity seamlessly.

Step 2: Message Parsing and Protocol Handling

Once messages arrive, the ticker plant must decode them. Exchanges use various protocols like ITCH, OUCH, FIX, or proprietary binary formats. The parsing layer extracts relevant fields from each message, identifying the symbol, price, quantity, timestamp, and message type.

This parsing happens at incredible speed. A high-performance ticker plant might parse millions of messages per second across multiple CPU cores. Some hardware-accelerated systems using FPGAs can parse messages in nanoseconds rather than microseconds, giving trading firms a measurable edge in speed-sensitive strategies.

Error handling is critical at this stage. Network glitches, exchange bugs, or malformed messages could corrupt downstream data. Robust ticker plants validate message integrity, handle sequence gaps, and detect anomalies before they propagate to trading systems.

Step 3: Market Data Normalization

Normalization transforms exchange-specific formats into a unified internal representation. Without this step, every downstream application would need custom code to handle each exchange feed. Normalization eliminates this complexity by creating a single, consistent data model.

For example, one exchange might represent prices in dollars and cents as integers (12550 for $125.50), while another uses decimal floating-point numbers. One might use Eastern Time, another UTC. One might identify stocks by ticker symbol, another by numeric security ID. The normalization layer converts all these variations into a standard format.

This standardization dramatically simplifies application development. A trading algorithm can consume normalized data from any exchange without modification. Risk systems can aggregate positions across venues using consistent symbology. The ticker plant absorbs the complexity of dealing with diverse exchange formats.

Step 4: Order Book Building

Perhaps the most sophisticated function of a ticker plant is building order books from raw market data. Exchanges send individual order events, but trading applications need a complete picture of the market. The ticker plant reconstructs this picture by maintaining real-time order books for every traded instrument.

Market data comes in different depths. Level 1 (L1) data includes just the best bid and ask prices. Level 2 (L2) adds the full order book, showing multiple price levels and their associated quantities. Level 3 (L3) provides individual order details, including participant identifiers and order IDs. The ticker plant must handle all these formats and make them available to subscribers.

Order book maintenance requires handling various event types. New orders arrive at specific price levels. Existing orders get modified or canceled. Trades execute against resting orders, removing liquidity. The ticker plant applies these changes in sequence, ensuring the book always reflects the current market state accurately.

Memory efficiency matters enormously here. A ticker plant tracking 10,000 symbols with full order book depth might maintain millions of price levels in memory. Sophisticated data structures like compressed sparse trees or hash maps enable nanosecond lookups while minimizing memory footprint.

Step 5: Distribution to Downstream Applications

The final stage delivers processed data to consumers. Different applications have different needs. A high-frequency trading engine might subscribe to every tick for a handful of symbols. A retail charting application might want second-by-second snapshots of thousands of stocks. A risk system might need position updates every minute.

Ticker plants support multiple distribution methods. Multicast broadcasting sends one copy of data to many subscribers efficiently. Unicast connections provide dedicated streams for latency-sensitive clients. Some systems offer filtered distribution, allowing subscribers to specify exactly which symbols and data types they want.

The distribution layer must handle slow subscribers gracefully. If one client cannot keep up with the data rate, the ticker plant must not let that client slow down everyone else. Common strategies include dropping messages for slow consumers, buffering data temporarily, or disconnecting problematic clients.

Latency Considerations at Every Stage

In modern markets, latency matters tremendously. A delay of just a few microseconds can mean the difference between profit and loss for high-frequency trading strategies. Ticker plants are engineered for speed at every processing stage.

Network interface cards optimized for kernel bypass eliminate operating system overhead. Lock-free data structures enable thread-safe concurrent access without contention. Memory-mapped files and zero-copy techniques minimize data movement. Some systems use dedicated hardware acceleration for parsing and normalization.

The total latency budget from exchange feed to client application typically ranges from 10 to 100 microseconds depending on the implementation. Software-based systems on commodity servers might achieve 50-100 microseconds. FPGA-based hardware systems can push this below 5 microseconds. Cloud-based implementations, while more flexible, often face higher latency due to network virtualization overhead.

Ticker Plant Architecture: Software vs Hardware

Not all ticker plants are built the same. The architecture choice depends on latency requirements, budget constraints, and operational preferences. Three main approaches dominate the industry today: software-based systems running on standard servers, FPGA-based hardware acceleration, and cloud-native implementations.

Software-Based Ticker Plants on Commodity Servers

Software ticker plants run on standard x86 servers with optimized network cards. They offer maximum flexibility and lower upfront costs. Development teams can modify logic quickly, deploy updates without hardware changes, and leverage existing DevOps infrastructure.

Modern software implementations achieve impressive performance. Using kernel bypass networking like DPDK or proprietary equivalents, they can process millions of messages per second with latencies in the 20-50 microsecond range. For many applications, including most algorithmic trading and risk management, this performance is more than adequate.

The kdb+ tick architecture exemplifies this approach. Built on the kdb+ time-series database and q programming language, it provides a complete ticker plant solution running entirely in software. The system includes a tickerplant process for ingestion and distribution, a real-time database (RDB) for current data, and a historical database (HDB) for archival storage.

FPGA-Based Ticker Plants

For the most latency-sensitive applications, FPGA-based ticker plants provide the ultimate speed. Field Programmable Gate Arrays are custom-programmed chips that process data in hardware rather than software. They can parse, normalize, and distribute market data in just a few nanoseconds.

Companies like NovaSparks and Exegy specialize in FPGA ticker plants. NovaTick, for example, normalizes 75 market data feeds into a single wire format that can be consumed directly by FPGAs or software applications. The hardware handles feed parsing, book building, and distribution with deterministic latency measured in single-digit microseconds.

The trade-off is flexibility. Changing FPGA logic requires hardware reconfiguration, which takes time and expertise. Costs are higher upfront, and ongoing maintenance requires specialized skills. These systems make sense primarily for high-frequency trading firms where microsecond advantages translate directly to profit.

Cloud-Based and Hybrid Approaches

Cloud computing has transformed many financial technology stacks, and ticker plants are no exception. Cloud-based implementations offer elastic scaling, global distribution, and reduced operational overhead. They are particularly attractive for firms without the infrastructure to manage physical hardware.

FactSet’s cloud ticker plant journey illustrates the potential. Starting from traditional data center deployments, they migrated their market data infrastructure to leverage cloud distribution networks. Using Infrastructure as Code (IaC) practices, they can spin up new points of presence globally in minutes rather than months.

The primary challenge is latency. Cloud virtualization adds network hops and processing overhead that can add hundreds of microseconds to the data path. For retail distribution and mid-frequency trading, this is acceptable. For ultra-low-latency strategies, cloud deployments remain challenging.

Hybrid architectures attempt to capture the best of both worlds. Critical latency-sensitive processing happens on dedicated hardware or bare-metal cloud instances. Distribution to global clients leverages cloud CDN networks. This approach balances speed with scalability.

Trade-offs: Cost, Latency, and Flexibility

Choosing the right architecture requires balancing competing priorities. Software systems offer the best cost-to-flexibility ratio. FPGA systems deliver unmatched speed at premium cost and reduced flexibility. Cloud solutions provide scalability and operational simplicity with higher baseline latency.

Most firms operate multiple ticker plant implementations for different use cases. High-frequency trading desks might use FPGA-based systems for execution while risk management uses software-based aggregation. Global distribution might flow through cloud infrastructure while core trading maintains dedicated hardware.

Real-World Ticker Plant Implementations

The scale of modern ticker plants is staggering. Major financial data providers process hundreds of billions of messages daily, distributing market data to millions of end users worldwide. Examining real implementations helps illustrate the practical challenges and solutions in this space.

Bloomberg: 200+ Billion Messages Daily

Bloomberg operates one of the largest ticker plant infrastructures in the world. Their systems ingest market data from over 350 exchanges and trading venues globally. During busy trading sessions, they process more than 200 billion messages per day.

This massive scale requires sophisticated distribution architecture. Bloomberg maintains points of presence in major financial centers worldwide. Data flows from exchanges into regional ticker plants, then distributes to local clients with minimal latency. Redundant systems ensure continuous availability even during exchange outages or network disruptions.

The Bloomberg Terminal, used by over 325,000 financial professionals, relies entirely on this infrastructure. Every price quote, chart update, and news alert flows through their ticker plant network. The system’s reliability has made it the industry standard for market data.

Major Exchanges and Their Requirements

Exchanges themselves run sophisticated ticker plant infrastructure to distribute their data. The Options Price Reporting Authority (OPRA) consolidates options data from multiple U.S. exchanges. During peak periods, OPRA generates over 100 million messages per second. Consuming firms must build ticker plants capable of handling this firehose without dropping data.

The NASDAQ TotalView feed provides full order book depth for all listed securities. With thousands of symbols and Level 3 data, the message rate can spike dramatically during volatile markets. Ticker plants must handle these “microbursts” without buffer overflows or message loss.

CME Group distributes futures and options data from the world’s largest derivatives exchange. Their market data platform supports both real-time feeds and historical replay. The ticker plants consuming CME data must handle diverse asset classes including equities, interest rates, commodities, and foreign exchange.

FactSet Cloud Migration Example

FactSet’s market data infrastructure transformation illustrates the cloud migration trend. Their ticker plant evolution started with traditional co-located hardware, then moved to hybrid deployments, and now leverages full cloud distribution for many workloads.

Their Infrastructure as Code approach enables rapid scaling. When a new exchange feed needs support, engineers can deploy the necessary infrastructure using automated templates. When OPRA volume spikes during market volatility, cloud auto-scaling adds capacity automatically.

FactSet’s implementation shows that cloud ticker plants can achieve impressive scale, even if they cannot match the microsecond-level latency of dedicated hardware. For many financial applications, the trade-off is worth it.

kdb+ Tick Architecture in Quant Trading

Many quantitative trading firms use the kdb+ tick architecture pioneered by KX Systems. This software-based approach has become a de facto standard in quantitative finance. The architecture separates concerns into distinct components that communicate via interprocess messaging.

The tickerplant component receives data from feed handlers and publishes to subscribers. It also logs every tick to a journal file for recovery and replay. The real-time database (RDB) maintains current market state in memory for fast querying. The historical database (HDB) stores older data on disk for research and backtesting.

Gateway processes handle client connections and query routing. The real-time engine (RTE) performs calculations on streaming data. Feed handlers connect to specific exchanges and convert their formats into the internal representation. This modular design allows firms to customize each component for their specific needs.

Why Ticker Plants Matter for Modern Trading?

Ticker plants might operate behind the scenes, but their importance to modern financial markets cannot be overstated. They provide the foundation upon which trillions of dollars in daily trading volume depends. Understanding their value helps explain why firms invest millions in optimizing these systems.

Latency Advantage in High-Frequency Trading

For high-frequency trading firms, every microsecond counts. The speed at which market data reaches trading algorithms directly impacts profitability. A firm that receives price updates 10 microseconds faster than competitors can react to market movements before prices adjust.

This latency arbitrage has driven massive investment in ticker plant optimization. Firms deploy FPGA-based systems, co-locate at exchanges, and use microwave networks to shave microseconds from data paths. The ticker plant sits at the center of this race, determining how quickly raw exchange data becomes actionable trading signals.

Even for less speed-sensitive strategies, latency matters. Portfolio managers making allocation decisions want current prices, not stale data. Retail traders executing orders need accurate bid-ask spreads. Risk managers monitoring positions require timely updates. The ticker plant’s speed affects every market participant.

Cost Efficiency Through Data Consolidation

Exchange data feeds are expensive. Each connection carries fees, and consuming raw feeds from dozens of exchanges would require massive infrastructure duplication. Ticker plants solve this by consolidating data centrally, then distributing normalized feeds to multiple consumers.

A single ticker plant can serve hundreds of downstream applications. Rather than each trading system connecting directly to exchanges, they connect to the ticker plant. This consolidation reduces exchange connection fees, simplifies network architecture, and eliminates redundant processing.

For large financial institutions, the cost savings run into millions of dollars annually. The ticker plant becomes a shared utility, amortizing infrastructure costs across many business units and applications.

Reliability During Market Volatility

Markets are unpredictable. During periods of extreme volatility, message volumes can spike 10x or more. Flash crashes, meme stock manias, and geopolitical events trigger massive surges in trading activity. Ticker plants must handle these bursts without faltering.

Robust ticker plants implement sophisticated load management. Buffer pools absorb temporary spikes. Slow subscriber protection prevents lagging clients from impacting the entire system. Automatic failover switches to backup systems if the primary fails. These mechanisms ensure continuous data flow when markets need it most.

During the GameStop trading frenzy in early 2021, many retail brokerage platforms experienced outages. Systems unable to handle the message volume failed just when traders needed them. Well-architected ticker plants with proper capacity planning maintained service through the chaos.

Regulatory Compliance and Audit Trails

Financial regulators require detailed records of trading activity. The SEC, FINRA, and other bodies mandate that firms maintain comprehensive audit trails. Ticker plants facilitate compliance by logging every market data message received and distributed.

The ticker plant log files serve as the definitive record of what market data was available at any given moment. If a trade dispute arises, firms can replay the exact data stream that their algorithms consumed. This replay capability proves that trading decisions were based on accurate information.

Modern ticker plants also support surveillance applications. By maintaining complete order book history, they enable trade reconstruction and pattern analysis. Compliance teams can investigate suspicious activity, reconstruct market conditions, and demonstrate regulatory adherence.

Competitive Edge for Trading Firms

In the competitive world of electronic trading, infrastructure quality differentiates winners from losers. Firms with superior ticker plants make better decisions faster. They see market movements before competitors. They manage risk more effectively. They provide better execution quality to clients.

This competitive dynamic drives continuous innovation. As one firm deploys faster hardware, others must match or exceed that performance. As cloud capabilities improve, firms experiment with hybrid architectures. The ticker plant has become a strategic asset, not merely a utility.

For retail investors, ticker plant quality indirectly affects trading costs. Brokers with better market data infrastructure can offer tighter spreads and faster execution. While individual traders may never see the ticker plant itself, they benefit from its capabilities every time they place an order.

Frequently Asked Questions

What is a ticker plant?

A ticker plant is a specialized system that aggregates market data from multiple financial exchanges, normalizes it into a standard format, and distributes it to trading applications in real-time. It acts as the central hub for market data processing, receiving raw feeds from exchanges and delivering clean, consistent information to downstream systems like trading algorithms, risk management platforms, and charting applications.

What is an example of ticker data?

Examples of ticker data include stock price quotes showing bid and ask prices, trade execution reports showing the price and quantity of completed transactions, order book updates showing changes to pending buy and sell orders, and market depth information displaying liquidity at various price levels. This data flows continuously during market hours, with modern exchanges generating millions of messages per second during active trading.

How does a ticker plant work?

A ticker plant works through five main stages: (1) Data ingestion from multiple exchanges via dedicated network connections, (2) Message parsing to decode exchange-specific protocols, (3) Normalization to convert diverse formats into a standard representation, (4) Order book building to reconstruct market state from individual events, and (5) Distribution to downstream applications using multicast or unicast delivery methods. The entire process typically completes in under 100 microseconds for high-performance systems.

How does the stock ticker work?

A stock ticker displays real-time price information for securities by receiving data from exchanges through a ticker plant infrastructure. When trades occur or orders change on an exchange, the ticker plant processes these events and pushes updates to connected displays. Modern electronic tickers show symbol, price, volume, and direction (up or down arrows), updating continuously as new market data arrives. The system can filter and format data for different audiences, from professional traders to retail investors.

What is the difference between a ticker plant and a feed handler?

A feed handler is a component that connects to a specific exchange feed and converts its protocol into a standard format. A ticker plant is the complete system that orchestrates multiple feed handlers, aggregates their output, maintains order books, and distributes data to subscribers. Think of feed handlers as the sensors that connect to exchanges, while the ticker plant is the central brain that processes and distributes the information. Many implementations combine both functions in a single system.

Why is low latency important in ticker plants?

Low latency is critical because trading decisions depend on having current market information. In high-frequency trading, microseconds matter. A firm receiving price updates even 10 microseconds faster than competitors can react to market movements before prices adjust, capturing profitable opportunities. Beyond speed-sensitive strategies, latency affects all market participants. Portfolio managers need current prices for decisions, risk systems need timely position updates, and execution algorithms need accurate bid-ask spreads to minimize trading costs.

Conclusion

Ticker plants represent the invisible infrastructure that makes modern financial markets possible. These systems process billions of messages daily, transforming raw exchange feeds into actionable intelligence for traders, risk managers, and investors worldwide. Understanding what a ticker plant is and how it processes market data reveals the complexity behind the simple stock prices we see on our screens.

The evolution of ticker plant technology reflects broader trends in computing. From the mechanical ticker tapes of the 1800s to today’s FPGA-accelerated and cloud-distributed systems, the fundamental mission remains unchanged: deliver accurate market data as quickly and reliably as possible. Yet the scale and sophistication have increased dramatically, with modern systems achieving latencies measured in single-digit microseconds.

As markets continue to electronic trading and data volumes grow, ticker plants will remain critical infrastructure. The ongoing race for speed, the migration to cloud architectures, and the integration of artificial intelligence for data processing all point to continued evolution. For anyone involved in financial markets, understanding ticker plants provides essential context about how information flows and why latency matters.

Whether you are building trading systems, managing market data infrastructure, or simply seeking to understand the technology behind stock prices, the concepts covered in this guide provide a solid foundation. The ticker plant may operate behind the scenes, but its impact on markets is front and center every trading day.