Net worth is the total value of everything you own minus everything you owe. It’s the single most accurate measure of your financial health, yet many people have never calculated their net worth or don’t understand what it tells them. In this guide, I’ll show you exactly how to calculate your net worth, explain what counts as assets and liabilities, and help you understand why this number matters more than your income or salary alone.

When I first calculated my net worth five years ago, I was surprised to discover that despite earning a good salary, my net worth was barely positive. That wake-up call completely changed how I approached money management. Since then, I’ve tracked my net worth quarterly and watched it grow from barely breaking even to building real wealth. The calculation itself takes just 15 minutes, but the insights it provides are invaluable.

Table of Contents

What is Net Worth?

Net worth is simply your assets minus your liabilities. This straightforward formula reveals your true financial position by showing what you’d have left if you sold everything you owned and paid off all your debts. Unlike income, which measures money flowing in, net worth measures wealth that has actually accumulated over time.

Net worth equals assets minus liabilities. This formula works for individuals, businesses, and even governments. Your net worth can be positive, meaning you own more than you owe, or negative, meaning your debts exceed your assets. A negative net worth doesn’t mean you’re failing financially—it’s common for young professionals with student loans to have negative net worth that improves over time.

The difference between net worth and income often confuses people. You might earn a high salary but have a low or negative net worth if you’re carrying significant debt. Conversely, someone with a modest income can build substantial net worth through saving and investing over time. Net worth captures the cumulative result of your financial decisions, not just your current earning power.

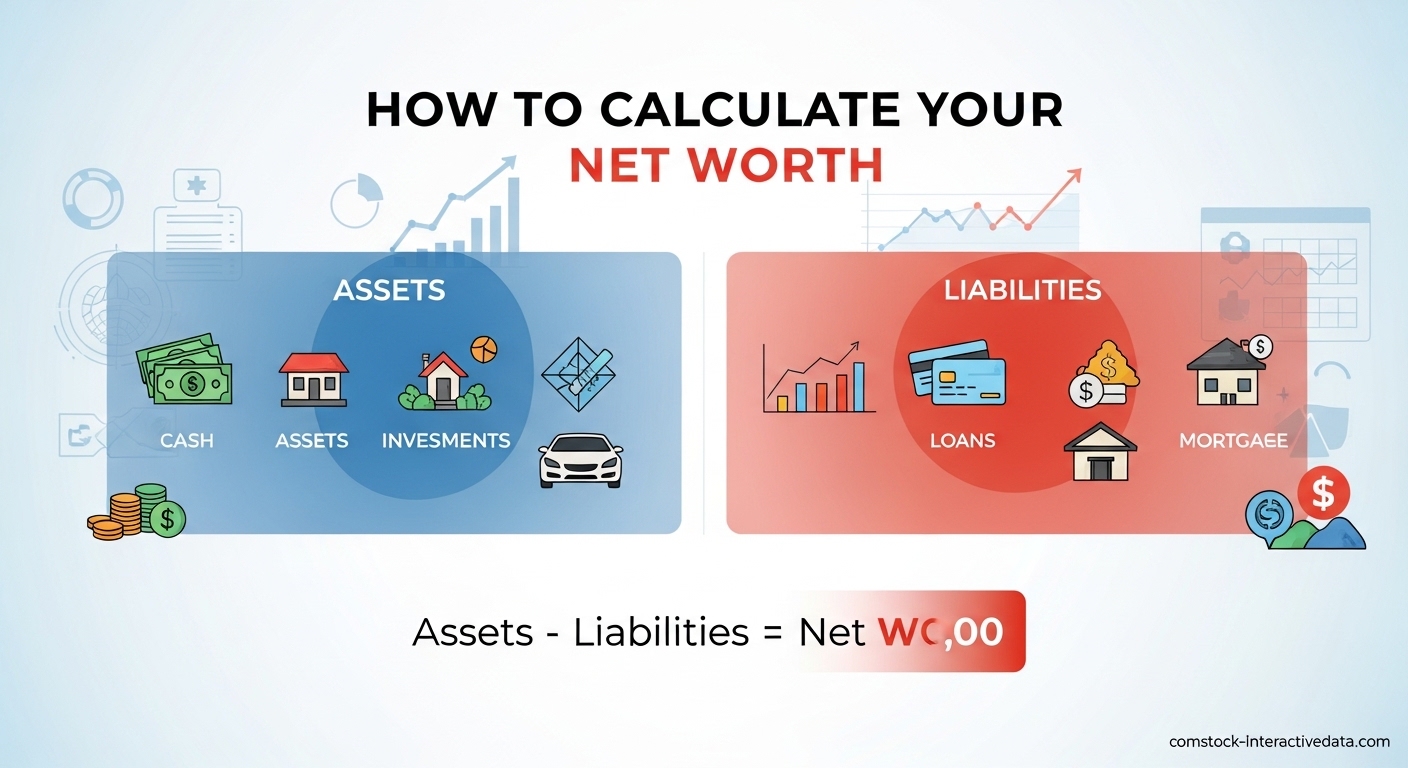

How to Calculate Your Net Worth?

Calculating your net worth involves two main steps: totaling your assets and totaling your liabilities. The process is straightforward, but accuracy matters. Here’s exactly how to do it.

Step 1: List all your assets. Start by making a complete inventory of everything you own. This includes cash in bank accounts, investment accounts, retirement accounts, real estate, vehicles, and valuable personal property. For each asset, use the current market value—not what you paid for it. Your home’s value is what it would sell for today, not what you purchased it for. Your car’s value is what you could get if you sold it now, not the sticker price.

Step 2: List all your liabilities. Next, list every debt you owe. This includes mortgage balances, auto loans, student loans, credit card balances, personal loans, and any other money you owe. For each liability, use the current payoff amount, not the original loan amount. Your mortgage balance is what you’d need to pay to own your home free and clear, not what you originally borrowed.

Step 3: Subtract liabilities from assets. Once you have both totals, subtract your total liabilities from your total assets. The result is your net worth. This simple calculation reveals whether you’re building wealth or accumulating debt, regardless of your income level.

Example calculation: Let’s say you have $25,000 in savings, $150,000 in retirement accounts, a home worth $350,000, and a vehicle worth $15,000. Your total assets equal $540,000. You owe $280,000 on your mortgage, $12,000 on your car, and $8,000 in credit card debt. Your total liabilities equal $300,000. Subtracting liabilities from assets ($540,000 – $300,000) gives you a net worth of $240,000.

This example shows why net worth matters more than income alone. You might earn $100,000 annually but have a net worth of $240,000 built over years, or you might earn the same amount but have a negative net worth due to debt and poor saving habits. Net worth captures the cumulative result of your financial decisions over time.

Understanding Your Assets

Assets are anything you own that has monetary value. When calculating your net worth, you’ll want to include all major assets, even those you’re still paying off. For example, if you own a home with a mortgage, the home’s full market value counts as an asset, while the remaining mortgage balance counts as a liability.

Liquid assets include cash and cash equivalents that can be quickly converted to cash without losing value. This includes checking accounts, savings accounts, money market accounts, and certificates of deposit. Liquid assets provide financial flexibility and emergency funds, so they’re especially important to track.

Investment assets include retirement accounts (401k, IRA, Roth IRA), taxable brokerage accounts, mutual funds, stocks, bonds, and other investments. Use the current market value for each investment account, not what you originally contributed. Investment accounts often represent the largest portion of net worth for people who have been saving consistently for years.

Real estate assets include your primary home, vacation properties, rental properties, and land. For each property, use the current market value based on recent comparable sales in your area, not the tax assessed value or what you paid. Real estate can be a significant asset class, but remember that property values fluctuate with market conditions.

Vehicle and personal property assets include cars, trucks, boats, RVs, and valuable personal property like jewelry, art, or collectibles. Use realistic market values for these items. Most vehicles depreciate over time, so your car might be worth less than you think. Personal property like furniture and clothing typically isn’t included unless it’s particularly valuable.

Understanding Your Liabilities

Liabilities are any debts or financial obligations you owe to others. When calculating net worth, include every liability regardless of whether it’s “good debt” or “bad debt.” A mortgage is still a liability even though it helped you purchase an appreciating asset.

Mortgage debt includes the remaining principal balance on your home, investment properties, or vacation homes. Use the payoff amount, not the original loan amount or your monthly payment. Mortgage debt is often the largest liability for homeowners, but it’s offset by the corresponding real estate asset.

Auto loan debt includes the remaining balance on car loans, truck loans, and loans for other vehicles. As with mortgages, use the current payoff amount. Auto loans typically have higher interest rates than mortgages, so they can slow net worth growth if you’re constantly carrying new car loans.

Credit card debt includes all balances on credit cards, store cards, and revolving credit lines. Credit card debt typically carries high interest rates, making it particularly damaging to net worth growth. Many people are surprised by how much credit card debt they’re carrying when they list it for net worth calculation.

Student loan debt includes federal and private student loans for undergraduate and graduate education. Student loan debt has become a major liability for many Americans, often delaying positive net worth for years after graduation. Include the total remaining balance across all student loans.

Personal loan debt includes personal loans from banks, credit unions, online lenders, and loans from family members. Personal loans often have high interest rates and can significantly impact your net worth calculation if not managed carefully.

Why Your Net Worth Matters?

Your net worth matters because it provides a complete picture of your financial health that income alone cannot reveal. A high income doesn’t guarantee financial security if you’re carrying substantial debt, while a modest income can still lead to significant wealth accumulation through consistent saving and investing. Net worth captures the cumulative result of your financial decisions over time.

Net worth serves as a progress tracker for your financial goals. Whether you’re building an emergency fund, saving for a down payment, or planning for retirement, your net worth shows whether you’re moving in the right direction. I’ve found that tracking my net worth quarterly keeps me motivated to make better financial decisions and celebrate progress that isn’t visible in my monthly budget.

Lenders and financial institutions consider your net worth when evaluating loan applications. A strong net worth demonstrates financial stability and reduces risk for lenders, potentially qualifying you for better interest rates on mortgages, auto loans, and business loans. Your net worth essentially measures your financial strength and borrowing capacity.

For retirement planning, net worth is especially critical. Social Security and pensions provide only a portion of retirement income, so your personal net worth must fill the gap. Financial planners often use net worth targets to determine retirement readiness, with common benchmarks suggesting having multiple times your annual salary saved by certain ages.

Positive versus negative net worth tells an important story about your financial trajectory. Positive net worth means you own more than you owe, indicating financial strength and the ability to weather emergencies. Negative net worth means your debts exceed your assets, which is common for young professionals but should improve over time as you pay down debt and build assets. The trend matters more than the current number—is your net worth increasing or decreasing over time?

Common Net Worth Calculation Mistakes

Many people make mistakes when calculating their net worth that lead to inaccurate results. Based on community discussions and financial forums, these errors are surprisingly common and can significantly distort your financial picture.

Using purchase price instead of market value: This is perhaps the most common mistake. Your home is worth what it would sell for today, not what you paid for it. Your car is worth its current resale value, not the sticker price. Using purchase price instead of market value can significantly overstate or understate your net worth. Always use current market values based on what you could actually get if you sold the asset today.

Forgetting retirement accounts: Many people overlook retirement accounts when calculating net worth, especially if they’re spread across multiple employers from different jobs. Your 401(k) balances, IRA balances, and pension vesting all count as assets. These accounts often represent significant wealth that’s easy to forget because it’s not accessible without penalty until retirement age.

Not including all debts: It’s tempting to leave smaller debts off your net worth calculation, but every liability counts. That $500 credit card balance, the personal loan from family members, and the medical bills in collections all reduce your net worth. Some people also forget to include the full balance of loans they’re actively paying down, listing only the monthly payment instead of the total owed.

Inconsistent tracking methodology: The most valuable aspect of net worth tracking is comparing your number over time to measure progress. This only works if you calculate it consistently using the same methodology. If you include your car’s value one quarter but exclude it the next, your trend line becomes meaningless. Pick a methodology and stick with it so you can accurately measure whether your net worth is growing.

Analysis paralysis: Some people get stuck trying to calculate the perfect net worth number, obsessing over whether to include personal belongings or how to value certain assets. Remember that consistency matters more than precision. It’s better to calculate a rough net worth number quarterly than to never calculate it at all because you’re trying to be perfect. Your net worth is a tool for tracking progress, not an exact accounting of every single thing you own.

How Often Should You Calculate Net Worth?

The frequency of net worth calculation depends on your goals and personality type. I calculate my net worth quarterly because monthly feels too frequent to show meaningful progress, while annually feels too infrequent to catch problems early. Many financial communities recommend quarterly or semi-annual calculation as a sweet spot.

The best time to calculate net worth is after major financial events or life changes. This includes after receiving a bonus or tax refund, after paying off a significant debt, after a major purchase like a home or car, or at the end of each calendar year. These milestones provide natural checkpoints for measuring financial progress.

For tracking methods, some people prefer spreadsheets where they can see trend lines over time, while others use apps that automatically sync with financial accounts. The best method is the one you’ll actually use consistently. I keep a simple spreadsheet with dates down the left column and asset categories across the top, making it easy to see whether each category is growing or shrinking over time.

What you should look for in your net worth calculation is the trend line over time, not just the current number. Is your net worth increasing or decreasing? Which assets are growing fastest? Are liabilities shrinking or growing? These trends reveal whether your financial strategy is working or needs adjustment.

Frequently Asked Questions

How is net worth calculated and why is it important?

Net worth is calculated by subtracting your total liabilities from your total assets. Net Worth = Assets – Liabilities. It’s important because it provides the most accurate measure of your financial health by showing what you actually own versus what you owe, regardless of your income level.

What is considered a good net worth by age?

Financial benchmarks suggest having 2x your annual salary by age 35, 3x by age 40, and 6x by age 50 for retirement readiness. However, these are general guidelines and individual circumstances vary significantly based on location, career path, family situation, and financial goals. Focus on your net worth trend over time rather than comparing to age-based targets.

Should I include my home in my net worth calculation?

Yes, include your home’s current market value as an asset and your remaining mortgage balance as a liability. Some financial planners recommend calculating both total net worth and liquid net worth (excluding your home and other illiquid assets) to get a complete picture of your financial position. Both numbers are useful for different purposes.

What is the difference between net worth and income?

Income is money flowing in through salary, business earnings, or investments, while net worth is the cumulative wealth you’ve built over time. You can have a high income but low net worth if you spend everything you earn, or a modest income but high net worth through years of saving and investing. Net worth measures wealth accumulation, not earning power.

How often should I recalculate my net worth?

Most financial experts recommend calculating net worth quarterly or semi-annually. Monthly is too frequent to show meaningful progress, while annually may miss opportunities to course-correct if needed. Choose a consistent schedule and stick with it so you can accurately measure your financial trajectory over time.

Conclusion

Calculating your net worth is one of the most powerful financial tools available, yet many people have never done it. This simple calculation—assets minus liabilities—reveals your true financial position and provides a baseline for measuring progress over time. Whether your net worth is positive or negative matters less than whether it’s trending in the right direction.

The process takes just 15 minutes but provides insights that can transform your financial decision-making. By understanding your net worth, you can make better choices about saving, investing, debt repayment, and major purchases. I encourage you to calculate your net worth today and commit to tracking it regularly. The number might surprise you, but the awareness it provides is invaluable for building real wealth over time.