A certificate of deposit (CD) is a type of savings account that pays a fixed interest rate on your deposit for a set period of time. If you have been wondering how do CDs work, you are not alone. Millions of savers use CDs to grow their money safely while earning higher returns than traditional savings accounts.

In this guide, I will explain everything you need to know about certificates of deposit. We will cover the mechanics of how CDs function, the different types available, and whether they are the right choice for your savings goals. By the end, you will understand exactly how to put your money to work with CDs.

Table of Contents

What Is a Certificate of Deposit?

A certificate of deposit is a time deposit offered by banks and credit unions. Unlike a regular savings account, you agree to leave your money untouched for a specific period called the term. In exchange, the bank pays you a guaranteed fixed interest rate that is typically higher than standard savings rates.

When you open a CD, you deposit a lump sum amount known as the principal. The bank locks in an annual percentage yield (APY) for the entire term. Your money earns compound interest throughout the term, meaning you earn interest on your interest. At the end of the term, called the maturity date, you receive your original principal plus all earned interest.

CDs are considered one of the safest savings vehicles available. They are insured by the Federal Deposit Insurance Corporation (FDIC) at banks or the National Credit Union Administration (NCUA) at credit unions. This insurance protects your deposits up to $250,000 per depositor, per institution.

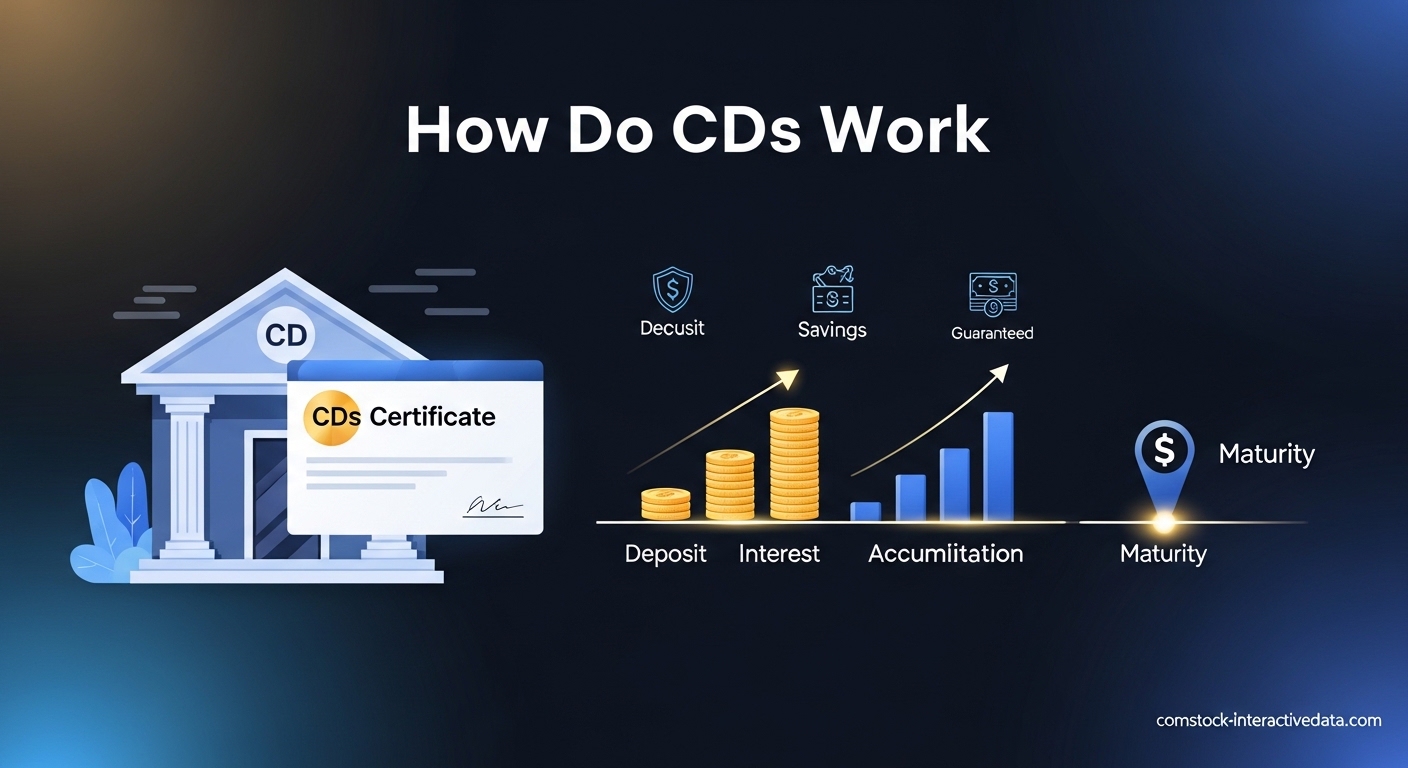

How Do CDs Work? The Complete Process

Understanding how do CDs work is straightforward once you break it down into steps. The process from opening a CD to receiving your money back follows a predictable pattern. Here is exactly what happens when you use a certificate of deposit.

Step 1: Choose Your CD and Make the Deposit

You start by selecting a CD that matches your savings timeline and goals. Banks offer CDs with terms ranging from 3 months to 5 years or longer. You deposit a lump sum, which can range from as little as $500 to $100,000 or more depending on the CD type.

Most banks require a minimum opening deposit, typically between $500 and $1,000. Some online banks offer no-minimum CDs, while jumbo CDs require deposits of $100,000 or more. The APY is locked at the time of opening and will not change regardless of market fluctuations.

Step 2: Interest Accrues During the Term

Once your CD is open, interest begins accruing immediately. The bank calculates interest based on your principal amount and the APY. Most CDs compound interest daily or monthly, which maximizes your returns.

For example, if you deposit $10,000 in a one-year CD with a 4% APY, you would earn $400 in interest over the full year. A $500 deposit in the same CD would earn $20 in interest. The interest adds to your principal throughout the term, creating a snowball effect.

Step 3: Wait Until Maturity

During the CD term, your money remains with the bank. You cannot withdraw funds without triggering an early withdrawal penalty. This commitment is what allows banks to offer higher rates than savings accounts.

Some banks offer no-penalty CDs that allow withdrawals without fees, though these typically pay lower rates. Standard CDs require you to wait until the maturity date to access your money without penalties. The maturity date is clearly stated when you open the CD.

Step 4: Receive Your Principal Plus Interest

When your CD reaches maturity, the bank returns your original deposit plus all accumulated interest. At this point, you have several options. You can withdraw all the money, renew the CD for another term, or roll over only the principal and withdraw the interest.

Most banks offer a grace period of 7 to 10 days after maturity during which you can make changes without penalty. If you do nothing, many CDs automatically renew at the current market rate. Always check the renewal terms to avoid getting locked into an unfavorable rate.

Understanding CD Terms and Maturity

The term length is one of the most important decisions when opening a CD. Terms typically range from 3 months to 5 years, though some banks offer CDs with terms as short as 1 month or as long as 10 years. The term you choose directly impacts your interest rate and liquidity.

Shorter-term CDs offer more flexibility but usually pay lower rates. A 3-month CD might pay 3% APY while a 5-year CD could pay 4% APY or higher. However, committing to a longer term means your money is locked away for years. If interest rates rise during that time, you could miss out on better opportunities.

The maturity date is the specific date when your CD term ends and you can access your money without penalty. Mark this date on your calendar. Missing the grace period after maturity could result in your CD automatically renewing for another full term, locking your money away again.

Types of CDs

Not all CDs work the same way. Banks offer several types of certificates of deposit to meet different savings needs. Understanding these variations helps you choose the right CD for your situation.

Fixed-Rate CDs

Fixed-rate CDs are the most common type. They offer a guaranteed interest rate that stays the same for the entire term. You know exactly how much you will earn when you open the CD. This predictability makes fixed-rate CDs popular for conservative savers.

Variable-Rate and Bump-Up CDs

Variable-rate CDs have interest rates that can change over time based on market conditions. Bump-up CDs give you the option to increase your rate once during the term if the bank raises rates on new CDs. These types protect you if interest rates rise after you open your CD.

No-Penalty CDs

No-penalty CDs, also called liquid CDs, allow you to withdraw your money before maturity without paying an early withdrawal penalty. These offer the safety of a CD with the flexibility of a savings account. The trade-off is that no-penalty CDs typically pay lower rates than standard CDs.

Jumbo CDs

Jumbo CDs require minimum deposits of $100,000 or more. In exchange for the larger commitment, banks often offer higher interest rates. Jumbo CDs are popular with high-net-worth individuals and businesses looking to park large amounts of cash safely.

IRA CDs

IRA CDs are held within an individual retirement account. They offer the tax advantages of an IRA combined with the guaranteed returns of a CD. IRA CDs are popular with retirees seeking to preserve capital while earning steady interest.

Brokered CDs

Brokered CDs are sold through brokerage firms rather than directly from banks. They often offer higher rates and can sometimes be sold on a secondary market before maturity. However, selling a brokered CD before maturity could result in a loss if interest rates have risen.

CD Rates Explained 2026

Understanding CD rates helps you maximize your returns. The annual percentage yield (APY) represents the total interest you will earn in one year, including the effects of compounding. A higher APY means more money in your pocket.

CD rates in 2026 have been influenced by Federal Reserve policy decisions. When the Fed raises the federal funds rate, banks typically increase CD rates to remain competitive. When rates fall, CD yields decline accordingly. Shopping around is essential because rates vary significantly between institutions.

Here is how to calculate your CD earnings. Multiply your deposit amount by the APY to find your annual interest. For a 6-month CD, divide the annual amount by 2. For a 3-month CD, divide by 4. A $10,000 CD at 4% APY earns $400 per year, $200 in 6 months, or $100 in 3 months.

Pros and Cons of CDs

Before opening a CD, consider both the advantages and disadvantages. CDs are excellent tools for specific situations but may not be right for everyone. Here is a balanced look at what CDs offer.

Advantages of CDs

CDs provide guaranteed returns. Unlike stocks or bonds, you know exactly how much you will earn when you open a CD. There is no market risk or volatility to worry about. Your principal is protected.

CDs are federally insured. FDIC insurance at banks and NCUA insurance at credit unions protect your deposits up to $250,000 per person, per institution. Even if the bank fails, your money is safe.

CDs typically pay higher rates than savings accounts. The trade-off of locking your money away is rewarded with better yields. In 2026, top CD rates often exceed 4% APY while regular savings accounts might pay less than 1%.

CDs help you avoid spending temptation. Because your money is locked away, you cannot easily access it for impulse purchases. This forced discipline helps you reach savings goals.

Disadvantages of CDs

The biggest negative of putting your money in a CD is illiquidity. Your money is locked away for the full term, and accessing it early triggers penalties. Unlike savings accounts, you cannot withdraw funds whenever needed without consequences.

Early withdrawal penalties can be severe. Most banks charge several months of interest for early withdrawals. On longer-term CDs, the penalty might equal 6 to 12 months of interest. In some cases, penalties can eat into your principal if you withdraw very early.

CDs may not keep pace with inflation. If inflation runs higher than your CD rate, your purchasing power actually decreases. Some critics call CDs “certificates of depreciation” because real returns can be negative after accounting for inflation.

You risk missing out on rising rates. If interest rates increase after you open a CD, you are stuck earning your original rate until maturity. Bump-up CDs offer some protection, but standard CDs do not.

Early Withdrawal Penalties Explained 2026

Understanding early withdrawal penalties is crucial before opening a CD. These penalties are the primary mechanism banks use to ensure you keep your money deposited for the agreed term. Breaking your commitment comes at a cost.

Early withdrawal penalties are typically calculated as a portion of the interest you would have earned. For CDs with terms of one year or less, the penalty is usually 3 months of interest. For longer-term CDs, penalties often equal 6 months to one year of interest.

Here is an example. Suppose you open a 2-year CD with a 4% APY and deposit $10,000. If you withdraw after 6 months, the bank might charge a penalty of 6 months interest, equal to $200. If you had only earned $200 in interest so far, the penalty wipes out all your earnings.

In extreme cases, penalties can exceed earned interest. If you withdraw very early from a long-term CD, you might lose part of your principal. Always check the specific penalty terms before opening a CD, and only deposit money you are confident you will not need during the term.

Are CDs Safe?

CDs are among the safest places to keep your money. The combination of federal insurance and guaranteed returns makes them low-risk savings vehicles. However, understanding the safety mechanisms helps you make informed decisions.

FDIC insurance protects bank deposits up to $250,000 per depositor, per institution, per ownership category. This means a single person can have $250,000 insured at one bank. Joint accounts receive $250,000 of coverage per co-owner. Credit union deposits receive identical protection through the NCUA.

You cannot lose money on a CD unless you withdraw early and incur penalties exceeding your earned interest. Even if your bank fails, the FDIC or NCUA ensures you receive your money back up to the insurance limits. This makes CDs safer than stocks, bonds, or even money market funds.

To maximize safety, stay within insurance limits. If you have more than $250,000 to deposit, spread it across multiple banks or different ownership categories. Consider using the NCUA or FDIC calculators to verify your coverage.

CD vs Savings Account: Which Is Better?

Choosing between a CD and a savings account depends on your financial situation and goals. Both are safe, insured savings vehicles, but they serve different purposes. Understanding the differences helps you decide where to keep your money.

Choose a CD when you have a specific savings goal with a known timeline. If you are saving for a down payment in two years, a 2-year CD locks in a guaranteed return. CDs are also good when you want to prevent yourself from dipping into savings for impulse purchases.

Choose a savings account when you need liquidity. Emergency funds should stay in savings accounts where you can access them immediately without penalties. If you might need the money unexpectedly, the flexibility of a savings account outweighs the higher rate of a CD.

High-yield savings accounts offer a middle ground. Online banks currently offer rates competitive with short-term CDs while maintaining full liquidity. In 2026, some high-yield savings accounts pay 4% or more APY, making them attractive alternatives to 3-month or 6-month CDs.

CD Ladder Strategy

A CD ladder is a strategy that spreads your money across multiple CDs with staggered maturity dates. This approach balances the higher rates of long-term CDs with the flexibility of having money mature regularly. Laddering is popular among retirees and conservative investors.

Here is how to build a basic CD ladder. Divide your total investment by the number of rungs you want. For example, with $10,000 and a 5-rung ladder, put $2,000 each into 1-year, 2-year, 3-year, 4-year, and 5-year CDs. Each year, one CD matures, and you reinvest it in a new 5-year CD.

The benefits of laddering are significant. You always have money becoming available within a year. You capture higher long-term rates on most of your money. If rates rise, you can invest the maturing CD at the new higher rate. If rates fall, you still have existing CDs locked at higher rates.

CD ladders work well for emergency funds beyond 3 months of expenses. They are also excellent for retirement income planning, allowing you to have predictable cash flows while earning better returns than savings accounts. The key is maintaining discipline and reinvesting maturing CDs to keep the ladder growing.

Frequently Asked Questions

How much does a $10,000 CD make in 6 months?

A $10,000 CD with a 4% annual percentage yield (APY) would earn approximately $200 in 6 months. Since CD rates are annualized, you calculate: $10,000 x 4% = $400 per year, divided by 2 for 6 months = $200.

What is the biggest negative of putting your money in a CD?

The biggest negative is illiquidity. Your money is locked away for the CD’s full term, and withdrawing early typically results in penalties that could eat into your principal. Unlike savings accounts, you cannot access your funds without penalty until maturity.

How much will a $10,000 3 month CD earn in 2026?

A $10,000 3-month CD at a 4.25% APY would earn approximately $106.25. Calculation: $10,000 x 4.25% = $425 annually, divided by 4 for 3 months = $106.25. Actual earnings depend on the current rate when you open the CD.

How much will a $100,000 CD make in one-year?

A $100,000 one-year CD at a 4% APY would earn $4,000 in interest. At a rate of 4.35%, a $100,000 CD would earn $4,350 after one year. Jumbo CDs of this size often qualify for the highest available rates.

Can you lose money on a CD?

You generally cannot lose your principal on a CD because they are FDIC or NCUA insured up to $250,000. However, you can lose money if you withdraw early and the penalty exceeds your earned interest. Inflation can also erode your purchasing power if the CD rate is below the inflation rate.

What happens when a CD matures?

When a CD matures, the bank returns your principal plus all earned interest. You typically have a grace period of 7-10 days to withdraw funds, transfer to another account, or renew the CD. If you take no action, many CDs automatically renew at the current market rate.

Conclusion

Understanding how do CDs work empowers you to make smarter savings decisions. Certificates of deposit offer a safe way to earn guaranteed returns on money you will not need for a specific period. With FDIC insurance protecting your deposits and fixed rates locking in your earnings, CDs provide peace of mind for conservative savers.

Before opening a CD, evaluate your liquidity needs, compare rates from multiple banks, and understand the early withdrawal penalties. Consider CD laddering for longer-term savings goals. With the knowledge from this guide, you are ready to put your money to work safely and effectively.