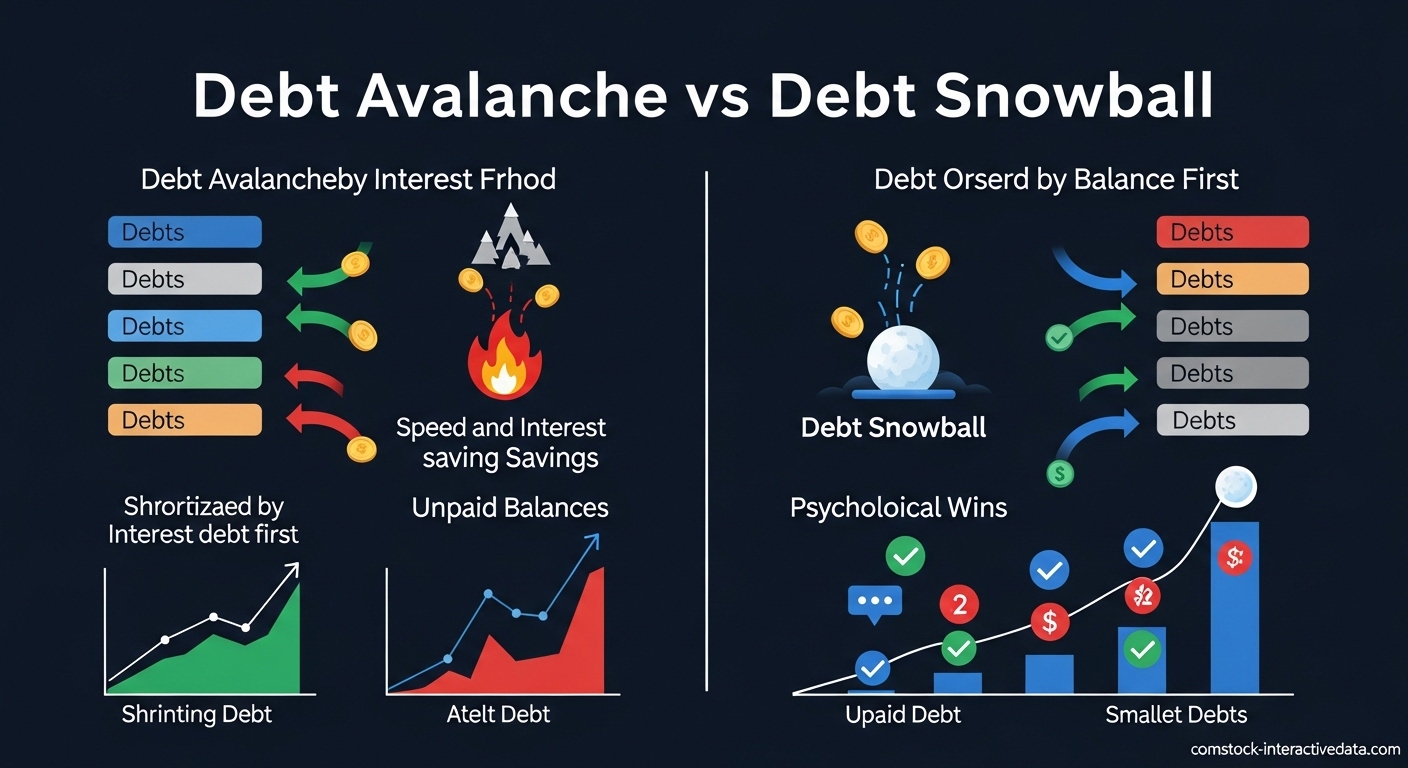

The debt avalanche and debt snowball are two proven debt payoff strategies that help you eliminate debt faster than making minimum payments alone. The debt avalanche prioritizes your highest-interest debts first to maximize interest savings, while the debt snowball focuses on your smallest balances first to deliver quick psychological wins and build momentum.

I have seen both methods work for different people. The avalanche method makes mathematical sense and saves you the most money. The snowball method recognizes that debt payoff is a marathon, not a sprint, and staying motivated matters just as much as the math.

This guide breaks down exactly how each method works, shows real numbers so you can see the difference, and helps you decide which approach fits your financial situation and personality. Let us dive into the details so you can start your debt-free journey with confidence.

Table of Contents

What Is the Debt Avalanche Method?

The debt avalanche method is a debt payoff strategy where you prioritize debts by interest rate, paying off the highest-rate debt first while making minimum payments on everything else. Once the highest-interest debt is eliminated, you roll that payment amount into the next highest-rate debt, creating an “avalanche” effect that accelerates your payoff.

This method is mathematically optimal. By targeting high-interest debt first, you minimize the total interest you pay over time. Credit cards with 20% APR or higher cost you significantly more than student loans at 5%, so eliminating the expensive debt first saves real money.

How the Debt Avalanche Method Works: 5 Steps

- List all your debts from highest interest rate to lowest, regardless of balance amount. Include credit cards, personal loans, student loans, auto loans, and any other debt.

- Continue making minimum payments on every debt to avoid late fees and credit score damage.

- Direct all extra money toward the debt with the highest interest rate. This is your target debt until it is paid off.

- Once the highest-interest debt is eliminated, take the entire payment you were making on it (minimum plus extra) and add it to the minimum payment of the next highest-interest debt.

- Repeat until debt-free, rolling payments down the list as each debt gets eliminated.

Debt Avalanche Example: Real Numbers

Here is a realistic scenario showing how the avalanche method works with three common debts. Imagine you have $500 per month to put toward debt payoff beyond minimum payments.

| Debt | Balance | Interest Rate | Minimum Payment |

|---|---|---|---|

| Credit Card A | $5,000 | 22% | $150 |

| Credit Card B | $3,000 | 18% | $90 |

| Student Loan | $10,000 | 6% | $200 |

With the avalanche method, you would put your extra $500 toward Credit Card A first (22% APR). Once that is paid off in about 9 months, you roll the $650 total ($150 minimum + $500 extra) toward Credit Card B. After eliminating that, you attack the student loan with $740 monthly.

Using the avalanche method, you would pay off all debt in approximately 28 months and pay around $2,100 in total interest. The key advantage: you attack the 22% debt first, preventing that high rate from compounding against you longer than necessary.

What Is the Debt Snowball Method?

The debt snowball method is a debt payoff strategy where you prioritize debts by balance size, paying off the smallest balance first regardless of interest rate. Popularized by Dave Ramsey, this method focuses on quick wins and psychological momentum over mathematical optimization.

The theory behind the snowball method is behavioral. Paying off a debt completely gives you an emotional boost and sense of accomplishment. This positive reinforcement helps you stick with your debt payoff plan when motivation wanes. For many people, the psychological benefit of closing accounts outweighs the mathematical advantage of the avalanche method.

How the Debt Snowball Method Works: 5 Steps

- List all your debts from smallest balance to largest, regardless of interest rate. Ignore the APR and focus only on the dollar amount owed.

- Continue making minimum payments on every debt to stay current and protect your credit score.

- Direct all extra money toward the debt with the smallest balance. This is your target debt until it is completely eliminated.

- Once the smallest debt is paid off, take the entire payment you were making on it and add it to the minimum payment of the next smallest debt. Your total monthly debt payment stays the same, but it grows in power as you eliminate debts.

- Repeat until debt-free, gaining momentum like a snowball rolling downhill as each small debt gets crushed.

Debt Snowball Example: Same Scenario

Using the exact same debt scenario as above, here is how the snowball method changes the payoff order. Remember, you still have $500 extra per month for debt payoff.

| Debt | Balance | Interest Rate | Minimum Payment | Snowball Order |

|---|---|---|---|---|

| Credit Card B | $3,000 | 18% | $90 | 1st (smallest balance) |

| Credit Card A | $5,000 | 22% | $150 | 2nd |

| Student Loan | $10,000 | 6% | $200 | 3rd (largest balance) |

With the snowball method, you attack Credit Card B first ($3,000 balance) because it is the smallest, even though it does not have the highest interest rate. You pay it off in about 5 months, giving you a quick win. Then you roll the $590 ($90 minimum + $500 extra) toward Credit Card A.

Using the snowball method, you would pay off all debt in approximately 29 months and pay around $2,400 in total interest. You pay slightly more interest than the avalanche method, but you eliminate your first debt 4 months faster, which many people find highly motivating.

Debt Avalanche vs Debt Snowball: Side-by-Side Comparison

Comparing these two debt payoff methods side-by-side helps clarify which approach suits your needs. The following table breaks down the key differences across several important dimensions.

| Factor | Debt Avalanche | Debt Snowball |

|---|---|---|

| Priority Order | Highest interest rate first | Smallest balance first |

| Primary Benefit | Saves the most money on interest | Quick wins build motivation |

| Payoff Timeline | Faster mathematically (usually 1-3 months) | Slightly longer, but feels faster initially |

| Interest Savings | Maximum savings | Moderate (typically $200-800 more than avalanche) |

| First Debt Payoff | Takes longer to eliminate first debt | Fastest path to first “debt-free” celebration |

| Best For | Disciplined people who trust the math | People who need motivation and visible progress |

| Psychological Impact | Requires patience; delayed gratification | Frequent wins; momentum building |

| Complexity | Requires tracking interest rates | Simple: just look at balance amounts |

Head-to-Head: Same Scenario Comparison

Here is how both methods perform using the example scenario from earlier ($18,000 total debt, $940 total monthly payments including $500 extra).

| Metric | Debt Avalanche | Debt Snowball | Difference |

|---|---|---|---|

| Time to first debt payoff | 9 months | 5 months | Snowball wins by 4 months |

| Total time to debt-free | 28 months | 29 months | Avalanche wins by 1 month |

| Total interest paid | $2,100 | $2,400 | Avalanche saves $300 |

| Number of debts eliminated in first year | 1-2 | 2 | Snowball wins |

In this scenario, the avalanche method saves you $300 and one month compared to the snowball method. However, the snowball method gives you a fully paid-off debt in just 5 months, while the avalanche method makes you wait 9 months for that first win.

Pros and Cons of Each Method

Both debt payoff strategies have legitimate advantages and drawbacks. Understanding these helps you make an informed choice based on your financial situation and personality type.

Debt Avalanche Pros and Cons

Pros:

- Saves the most money: By targeting high-interest debt first, you minimize total interest paid over the life of your debt payoff journey. On large debt loads with high APRs, this can save thousands of dollars.

- Mathematically optimal: The avalanche method is objectively the most efficient way to pay off debt from a pure numbers perspective.

- Faster total payoff: Because you pay less interest, you typically become debt-free 1-3 months sooner than with the snowball method.

- Works well for disciplined people: If you are motivated by logic and can stick to a plan without emotional reinforcement, this method rewards your discipline.

Cons:

- Delayed gratification: If your highest-interest debt is also your largest balance, you might wait months or even years before paying off your first debt completely. This can be demoralizing.

- Requires willpower: Without the psychological boost of quick wins, some people struggle to maintain motivation and abandon their debt payoff plan.

- More complex tracking: You need to monitor interest rates and potentially recalculate if rates change (especially with variable-rate credit cards).

Debt Snowball Pros and Cons

Pros:

- Quick psychological wins: Paying off your first debt quickly provides a tangible sense of accomplishment and proves that debt freedom is possible.

- Builds unstoppable momentum: Each debt you eliminate increases your payment power on the next debt, creating a snowball effect that feels increasingly powerful.

- Simple to implement: You only need to look at balance amounts, not interest rates or complex calculations. Just pay off the smallest debt first.

- Higher completion rates: Research suggests people using the snowball method are more likely to stick with their debt payoff plan long-term because of the positive reinforcement.

Cons:

- Costs more in interest: By ignoring interest rates, you may pay more over time, especially if you have high-APR credit cards with large balances that sit unpaid while you clear smaller debts.

- Slightly longer timeline: You typically become debt-free 1-3 months later than with the avalanche method, though the difference is usually small.

- Not mathematically optimal: Purely by the numbers, you are leaving money on the table compared to the avalanche approach.

Which Debt Payoff Method Is Better?

The honest answer: it depends on your financial situation and psychological makeup. Neither method is universally “better” for everyone. The best debt payoff strategy is the one you will actually stick with until you are debt-free.

Choose the debt avalanche method if you have high-interest credit card debt (APR above 15%), are naturally disciplined and motivated by logic, have a stable income that supports a long-term plan, and care more about total money saved than quick wins.

Choose the debt snowball method if you have struggled with debt payoff before, need visible progress to stay motivated, have several small debts you could eliminate quickly, or value psychological wins over mathematical optimization.

What Real People Say: Forum Insights

Our team analyzed discussions from Reddit communities like r/DaveRamsey, r/debtfree, and r/personalfinance to understand real experiences with both methods. The consensus: success depends on your personality.

Many Reddit users report that the snowball method kept them motivated and they paid off more debt overall than when they tried the avalanche method. Users consistently mention the psychological boost of closing accounts completely. However, users with very high-interest credit card debt (20%+ APR) often found the avalanche method saved them significant money and was worth the delayed gratification.

Interestingly, several users reported starting with the avalanche method but switching to snowball mid-journey when they felt their motivation slipping. This hybrid approach can work if you start with the math but switch to psychology when needed.

Decision Framework: 4 Key Questions

Ask yourself these questions to choose your method:

- What are my interest rates? If you have credit cards at 20%+ APR, the avalanche method becomes more compelling because the interest savings are substantial.

- How is my self-discipline? Be honest. If you have struggled to stick with financial plans before, the snowball method’s quick wins may be essential.

- What are my debt balances? If you have several small debts under $1,000 and one large high-interest debt, the snowball method gives you multiple quick wins before tackling the big one.

- What motivates me more: saving money or making progress? There is no wrong answer. Some people are driven by watching their total debt drop fastest; others need the satisfaction of eliminating individual debts completely.

Frequently Asked Questions

Which is better for paying off debt, snowball or avalanche?

Neither method is universally better. The avalanche method saves more money on interest and pays off debt faster mathematically. The snowball method provides quicker psychological wins and higher completion rates. Choose avalanche if you are disciplined and motivated by logic. Choose snowball if you need visible progress to stay motivated. The best method is the one you will stick with until debt-free.

Which debt payoff method is best?

The best debt payoff method depends on your personality and financial situation. If you have high-interest credit card debt (above 15% APR) and are naturally disciplined, the avalanche method is best because it saves the most money. If you struggle with motivation or need quick wins to stay committed, the snowball method is best because it builds momentum through psychological victories. Research suggests the snowball method has higher completion rates.

Does Dave Ramsey recommend snowball or avalanche?

Dave Ramsey strongly recommends the debt snowball method. He argues that personal finance is 80% behavior and 20% math. Ramsey believes the psychological boost of quick wins matters more than the mathematical optimization of interest savings. His Financial Peace University program teaches the snowball method exclusively, advocating that momentum and motivation are key to becoming debt-free.

Why would anyone use the snowball method instead?

People use the snowball method because it delivers quick psychological wins by eliminating small debts first. This momentum keeps them motivated during a long debt payoff journey. Research shows higher completion rates with the snowball method. The method is also simpler to implement since you only track balances, not interest rates. For many, the emotional satisfaction of closing accounts outweighs the extra interest paid.

Is snowball faster than avalanche?

No, the avalanche method is typically 1-3 months faster than the snowball method for total debt payoff because it minimizes interest costs. However, the snowball method is faster at delivering your first completely paid-off debt, which usually happens 2-4 months sooner than with the avalanche method. If you define speed as time to first win, snowball wins. If you define speed as time to total debt freedom, avalanche wins.

Should I use the snowball or avalanche method for debt?

Use the avalanche method if you have high-interest credit card debt (15%+ APR), are disciplined, and care most about saving money. Use the snowball method if you need motivation, have struggled with debt payoff before, or have several small debts you can eliminate quickly for wins. Consider a hybrid approach: start with avalanche for high-interest debt, then switch to snowball if motivation drops. Calculate both methods for your specific debts using an online calculator before deciding.

Conclusion: Start Your Debt-Free Journey Today

Both the debt avalanche and debt snowball methods work. The avalanche method saves you money by targeting high-interest debt first. The snowball method keeps you motivated by delivering quick wins on small balances. Your job is not to find the “perfect” method but to choose one and commit to it.

Calculate both approaches for your specific debts. If the interest savings from the avalanche method are substantial (over $500), lean toward that approach if you can handle the delayed gratification. If the difference is small or you know you need psychological reinforcement, choose the snowball method and trust the process.

The most important step is starting today. List your debts, choose your method, make a budget that includes extra payments, and take action. Whether you choose debt avalanche vs debt snowball, both paths lead to the same destination: financial freedom. Your debt-free future starts with the first payment you make above the minimum.