Managing money feels overwhelming when you do not know where to start. I remember staring at my bank account, wondering why my paycheck disappeared so fast every month. The 50/30/20 budget rule changed everything for me. This simple budgeting framework divides your income into three clear categories: needs, wants, and savings.

In this guide, I will walk you through exactly how the 50/30/20 rule works. You will learn what counts as a need versus a want, how to calculate your numbers, and real strategies for making this system fit your life. Whether you are creating your first budget or looking for a simpler method, this percentage-based approach gives you a clear starting point.

Table of Contents

What Is the 50/30/20 Budget Rule?

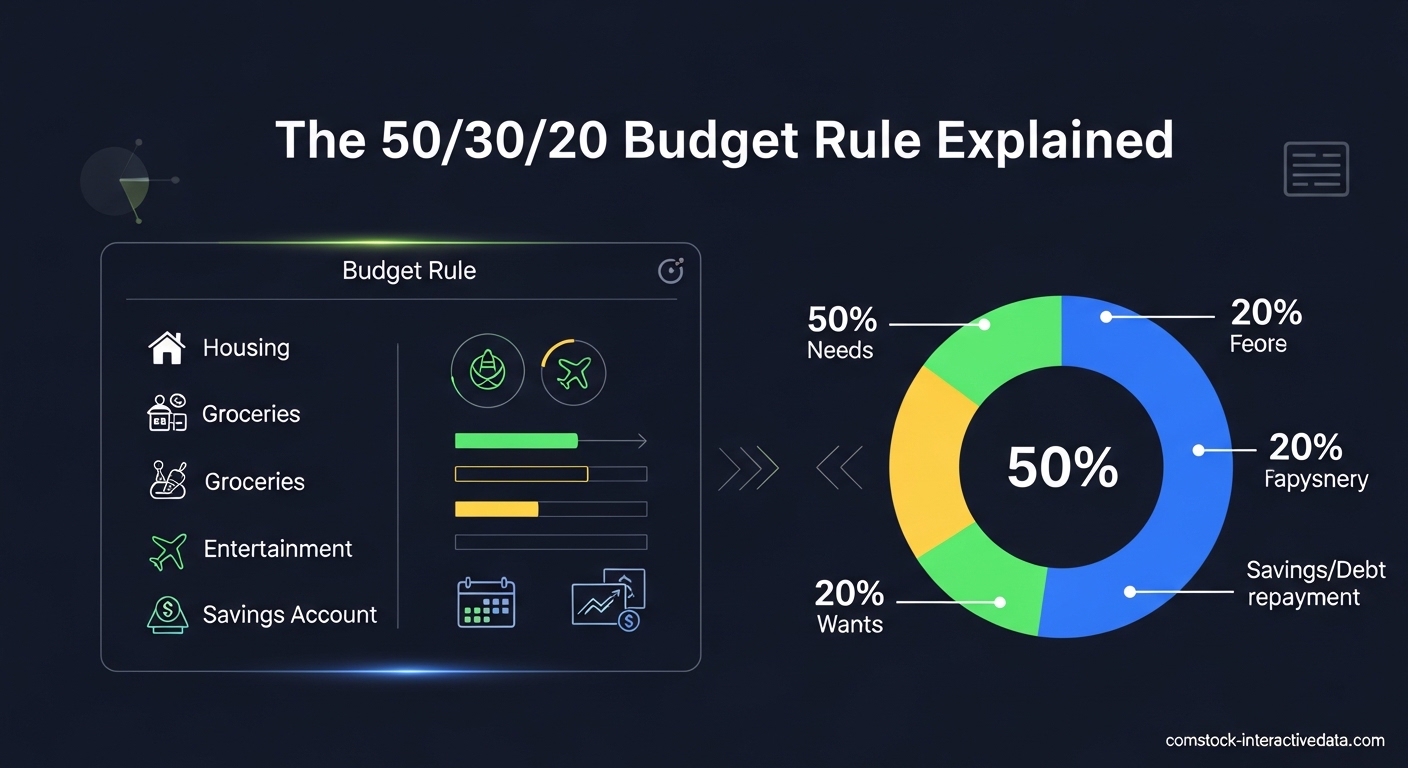

The 50/30/20 rule recommends putting 50% of your after-tax income toward needs, 30% toward wants, and 20% toward savings and debt repayment. This budgeting framework creates a balanced approach to money management without requiring complex spreadsheets or tracking every single purchase.

Senator Elizabeth Warren and her daughter Amelia Warren Tyagi popularized this method in their 2026 book “All Your Worth: The Ultimate Lifetime Money Plan.” They developed this approach after researching how families could build financial security without feeling deprived. The beauty lies in its simplicity: three categories, clear percentages, and no guilt about spending money on things you enjoy.

Unlike rigid budgeting systems that track every dollar, the 50/30/20 rule gives you flexibility within each category. You decide what matters most in your wants category. You choose how to split your savings between emergency funds and investments. This framework respects your individual priorities while ensuring you cover essentials and build wealth.

Understanding Your Income: After-Tax vs. Gross Pay

Before applying the 50/30/20 rule, you need to calculate your after-tax income correctly. This means using your take-home pay, not your gross salary. Look at your paycheck or bank statement for the amount that actually hits your account after taxes, health insurance, and retirement contributions come out.

For example, if you earn $60,000 per year gross, your after-tax income might be closer to $45,000 depending on your tax bracket and deductions. Divide that annual number by 12 to get your monthly take-home pay: approximately $3,750. This is the number you apply the percentages to.

Freelancers and gig workers with irregular income should calculate a 3-month or 6-month average. Use your lowest earning month as your baseline to ensure you never budget beyond your means. When you have a high-income month, resist the urge to inflate your wants category proportionally.

The 50%: Needs Category

Needs include expenses you cannot avoid without serious consequences. These are the bills and obligations that keep a roof over your head, food on your table, and your basic life functioning. If you cannot eliminate an expense without major disruption, it belongs in this category.

Common needs include:

- Housing: Rent or mortgage payments, property taxes, homeowners insurance

- Utilities: Electricity, water, gas, internet, phone service

- Food: Groceries and essential household supplies

- Transportation: Car payments, insurance, gas, public transit passes

- Healthcare: Insurance premiums, prescriptions, necessary medical visits

- Minimum debt payments: Credit card minimums, student loan minimums, any payment required to avoid default

The biggest challenge many people face: housing costs in expensive cities often push this category beyond 50%. If your rent alone consumes 45% of your income, you may need to adjust the percentages. I will cover modifications later in this guide.

The 30%: Wants Category

Wants include everything you could live without if necessary, but that makes life enjoyable. This category often confuses people because some “wants” feel essential to daily life. The key question: could you survive and maintain basic functioning without this expense?

Common wants include:

- Dining out: Restaurants, coffee shops, takeout, food delivery

- Entertainment: Streaming services, movie tickets, concerts, hobbies

- Subscriptions: Gym memberships, magazine subscriptions, premium app features

- Travel: Vacations, weekend trips, hotel stays

- Shopping: Clothing beyond necessities, electronics, home decor

- Personal care: Salon services, spa treatments, non-essential grooming

Here is where the 50/30/20 rule offers something most budgets do not: psychological permission to spend. Many budgeting methods make you feel guilty about every non-essential purchase. This framework explicitly allocates 30% of your money for enjoyment. You are not overspending; you are following the plan.

I found this permission especially helpful when I started budgeting. Knowing I had $450 dedicated to wants each month meant I could buy concert tickets without anxiety. The money was already accounted for in my plan.

The 20%: Savings Category

The savings category covers both building wealth and accelerating debt payoff beyond minimum payments. This 20% allocation creates your financial safety net and future security. Ignore this category, and you stay one emergency away from crisis.

Your 20% savings might include:

- Emergency fund: 3-6 months of expenses in an accessible savings account

- Retirement savings: 401(k) contributions beyond employer match, IRA deposits

- Extra debt payments: Paying above minimums on credit cards, loans, or mortgages

- Investment accounts: Brokerage accounts, index funds, other investments

- Specific goals: Down payment savings, education fund, major purchase fund

Financial experts generally recommend building your emergency fund first. Aim for $1,000 as a starter emergency fund, then expand to one month of expenses, then three months. Once you hit that milestone, shift focus to retirement savings while maintaining your emergency cushion.

High-yield savings accounts work best for emergency funds because they offer better interest rates than traditional savings while keeping your money accessible. For retirement and long-term investments, consider tax-advantaged accounts like 401(k)s and IRAs before taxable brokerage accounts.

How to Implement the 50/30/20 Rule: Step-by-Step

Getting started with this budgeting method takes about two hours of focused work. Follow these steps to set up your system and begin tracking.

Step 1: Calculate Your After-Tax Income

Look at your last three pay stubs or bank deposits. Add them up and divide by three to get your average monthly take-home pay. For freelancers, use a six-month average and work with your lowest earning month as your baseline.

Step 2: Apply the Percentages

Multiply your after-tax income by 0.50, 0.30, and 0.20 to get your target amounts for each category. Write these numbers down. For example, with $4,000 monthly take-home pay, you get $2,000 for needs, $1,200 for wants, and $800 for savings.

Step 3: Track Your Current Spending

Review the last 30 days of transactions from your bank and credit cards. Categorize each expense as need, want, or savings/debt payment. Do not judge yourself during this step. You are gathering data, not evaluating performance.

Step 4: Compare Reality to Targets

Add up your actual spending in each category. Compare these totals to your target percentages. Most people discover they spend far more than 50% on needs or far less than 20% on savings. This gap shows you exactly where adjustments must happen.

Step 5: Make Adjustments Over Time

You will not hit these percentages perfectly in month one. Focus on incremental improvements. If you currently save 5%, aim for 10% next month, then 15%, then 20%. Small progress beats perfect plans you abandon after two weeks.

Real Example: $3,500 Monthly Income Breakdown

Let me show you exactly how this looks with real numbers. I chose $3,500 because it represents a realistic take-home pay for many Americans earning $50,000 to $55,000 annually.

Monthly After-Tax Income: $3,500

- Needs (50%): $1,750

- Rent: $1,100

- Utilities: $150

- Groceries: $300

- Transportation: $150

- Phone: $50

- Wants (30%): $1,050

- Dining out: $300

- Streaming services: $50

- Entertainment: $200

- Shopping: $300

- Gym membership: $50

- Miscellaneous: $150

- Savings (20%): $700

- Emergency fund: $350

- 401(k) contribution: $250

- Extra debt payment: $100

This example assumes relatively modest housing costs. In high-cost cities, that $1,100 rent might jump to $1,800 or more. When that happens, you need to either increase your needs percentage temporarily or find ways to reduce other essential expenses.

Benefits of Using the 50/30/20 Rule

After three years of using this system, I have experienced several advantages that keep me committed to the framework.

Simplicity reduces decision fatigue. You do not need to categorize 47 different budget line items or track every coffee purchase. Three categories mean three decisions when reviewing your spending. This simplicity helps beginners stick with budgeting long enough to see results.

Built-in balance prevents burnout. Many extreme budgeting methods force you to cut all wants and live miserably for years. The 30% wants allocation acknowledges that money exists to support a life you enjoy, not just to survive. This balance makes the system sustainable over decades, not just months.

Automatic wealth building. By dedicating 20% to savings automatically, you create wealth without constant willpower battles. Set up automatic transfers on payday so the money moves before you can spend it. After six months, you will be amazed at your account balances.

Flexibility accommodates life changes. When your income increases, all three categories grow proportionally. When you face an unexpected expense, you know exactly which category to pull from. This adaptability serves you better than rigid systems that break under real-world pressure.

Limitations and When to Modify the Rule

The 50/30/20 rule provides an excellent starting framework, but it does not fit every situation perfectly. Understanding when and how to adjust the percentages helps you adapt this method to your reality.

High Cost of Living Areas

If you live in San Francisco, New York, Boston, or similar cities, your housing costs alone might consume 40-50% of your income. In these cases, a strict 50/30/20 split becomes impossible. Consider a 60/20/20 split temporarily: 60% needs, 20% wants, 20% savings. As your income grows, work toward the original proportions.

Low Income Situations

When you earn just enough to cover basic needs, saving 20% feels impossible. Start with whatever you can manage, even 5%. Focus first on building a small emergency fund, then gradually increase your savings rate as you advance in your career or reduce expenses.

Irregular Income Challenges

Freelancers, commissioned salespeople, and gig workers face unique budgeting challenges. During high-income months, save aggressively to cover low-income periods. Calculate your baseline needs (the minimum to survive) and ensure you maintain an emergency fund covering 6+ months of these essentials.

Aggressive Debt Payoff Goals

If you carry high-interest credit card debt, you might temporarily flip the wants and savings percentages. Try a 50/20/30 split where you allocate 30% to debt payoff and savings. Eliminating 20% APR debt faster saves more money than earning 4% in a savings account.

Different Life Stages

Young professionals early in their careers might prioritize experiences and travel, allocating more to wants temporarily. Parents with children often see needs consume more than 50% due to childcare costs. Retirees may shift their entire framework since they are drawing down savings rather than building them.

Alternative Budgeting Methods to Consider

If the 50/30/20 rule does not fit your situation, several alternatives exist. Understanding these options helps you choose the right framework for your specific circumstances.

The 60/30/10 Rule

This variation works better for people in high cost-of-living areas or those early in their careers. You allocate 60% to needs, 30% to wants, and 10% to savings. While the lower savings rate slows wealth building, it acknowledges financial reality for many people starting out.

The 40/30/20/10 Rule

This method adds a fourth category: 40% needs, 30% wants, 20% savings, and 10% debt payoff or giving. People with significant debt or those who tithe often prefer this structure because it separates charitable giving or aggressive debt elimination from general savings.

Zero-Based Budgeting

Every dollar gets assigned a job before the month begins. Income minus expenses equals zero. This method offers maximum control but requires more time and discipline. Popularized by You Need A Budget (YNAB), this approach works well for detail-oriented people who enjoy granular tracking.

Envelope System

Withdraw cash for each spending category and place it in labeled envelopes. When an envelope empties, spending in that category stops until next month. This physical system creates powerful psychological barriers to overspending and works exceptionally well for people struggling with credit card debt.

Tools and Apps That Support the 50/30/20 Rule

You do not need expensive software to implement this budgeting method. Several free and low-cost tools help you track your three categories without overwhelming complexity.

Spreadsheets: A simple Google Sheets or Excel document works perfectly. Create three columns for needs, wants, and savings. Enter your transactions weekly and watch the totals. I used this method for my first year and found it surprisingly effective.

Budgeting apps: Many popular apps allow custom categories that align with the 50/30/20 framework. Look for apps that let you set percentage targets and alert you when you approach category limits. Some automatically categorize transactions, saving you significant time.

Banking features: Many modern banks offer built-in budgeting tools that categorize spending automatically. Some even let you create sub-accounts or “buckets” for different purposes, effectively creating digital envelopes for your needs, wants, and savings.

Manual tracking: A notebook and pen still work beautifully. Write down every expense as it happens and categorize it immediately. The physical act of recording spending creates awareness that automated systems sometimes lack.

Frequently Asked Questions

How to use the 50/30/20 budget rule?

Calculate your after-tax income, then allocate 50% to needs (housing, food, utilities), 30% to wants (entertainment, dining out, hobbies), and 20% to savings and debt repayment. Track your spending for 30 days to see where you currently stand, then adjust your habits gradually to match these percentages.

What are the downsides of the 50/30/20 rule?

The main downsides include difficulty applying it in high cost-of-living areas where housing alone exceeds 50%, challenges for people with irregular income, and the possibility that 20% savings may not be enough for those starting to save later in life. The rule also does not account for significant debt burdens that may require more aggressive payoff strategies.

Does the 50/30/20 rule actually work?

Yes, the rule works well for many people, especially budgeting beginners and those with stable incomes in moderate cost-of-living areas. Success depends on accurately categorizing expenses and adjusting the percentages when necessary. The framework provides structure while maintaining enough flexibility for real-world application.

What are three disadvantages of using the 50/30/20 budget?

First, housing costs in expensive cities often make the 50% needs allocation unrealistic. Second, the rule does not specifically address high-interest debt payoff, which should sometimes take priority over savings. Third, people with irregular income find it challenging to apply fixed percentages when their monthly earnings fluctuate significantly.

Conclusion: Start Your 50/30/20 Journey Today

The 50/30/20 budget rule offers a proven framework for managing your money without overwhelming complexity. By dividing your after-tax income into needs, wants, and savings, you create a sustainable system that covers essentials, allows enjoyment, and builds wealth simultaneously.

Remember that perfection matters less than progress. If you cannot hit the exact percentages immediately, start where you are and improve gradually. The goal is developing awareness about where your money goes and making intentional choices about your financial future.

Take the first step today: calculate your after-tax income and apply the percentages. Track your spending for just one week. That small action starts a journey toward financial clarity and confidence that will serve you for decades to come.