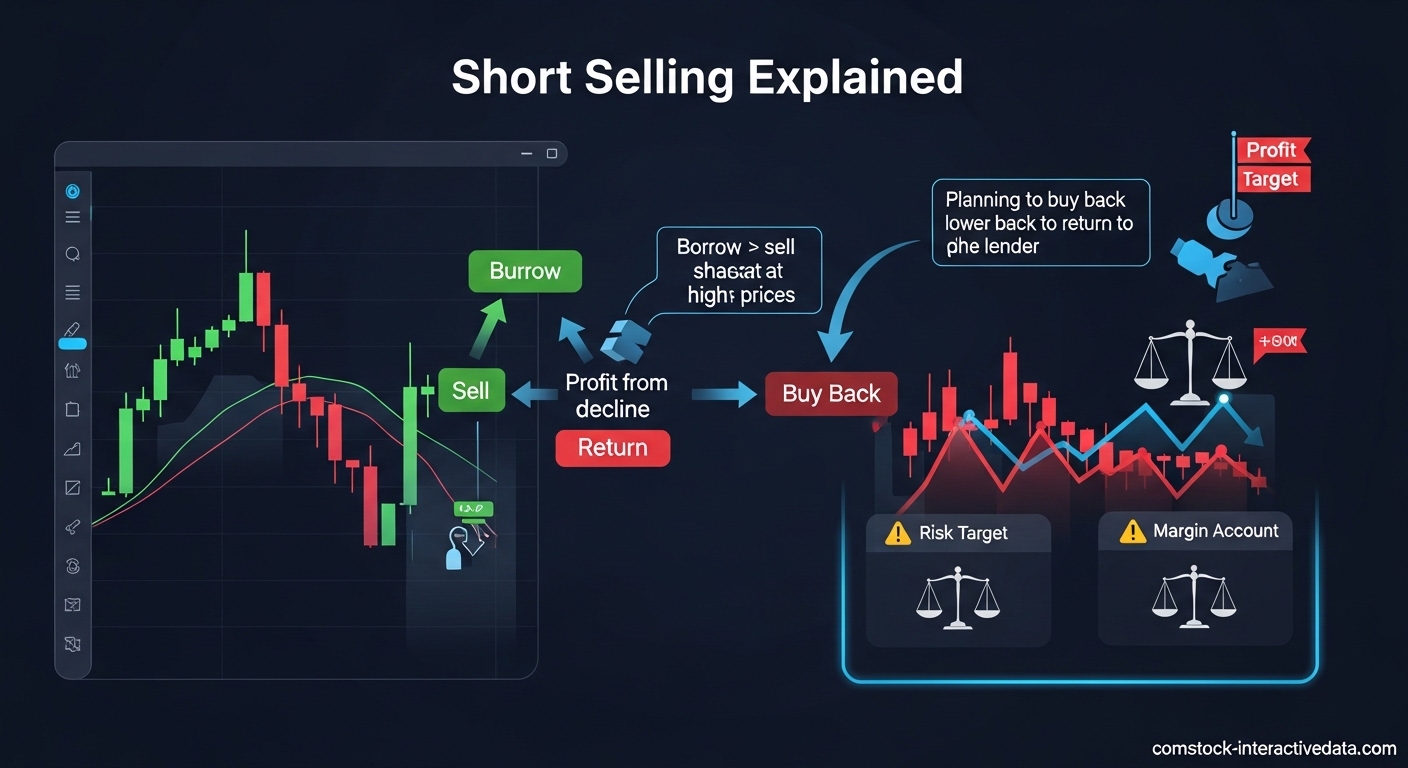

Short selling is a trading strategy where investors borrow shares of a stock they believe will decline in price, sell them on the open market, and later buy them back at a lower price to return to the lender. The difference between the sale price and repurchase price represents the profit, minus any borrowing fees.

Most investors only profit when stocks go up. But what if you could make money when prices fall? That is exactly what short selling allows you to do. It sounds counterintuitive at first, selling something you do not own. Yet this strategy has been used by professional traders and hedge funds for decades to profit during market downturns, hedge existing positions, and even expose corporate fraud.

Our team has analyzed short selling strategies across multiple market cycles. We have seen traders generate significant returns during bear markets. We have also watched inexperienced investors lose their entire accounts because they did not understand the risks. This guide will teach you everything you need to know about short selling, from the basic mechanics to advanced risk management techniques.

By the end of this article, you will understand exactly how short selling works, the step-by-step process to execute a short trade, the significant risks involved, and whether this strategy fits your investment goals. You will also learn about tax implications that most guides ignore, and discover safer alternatives if short selling proves too risky for your situation.

Table of Contents

What Is Short Selling?

Short selling, also called shorting or going short, is an investment strategy where you sell a security you have borrowed, intending to buy it back later at a lower price. Instead of buying low and selling high, you sell high first and buy low later. This reversal of the traditional buy-sell order is what makes short selling unique.

The mechanism works through borrowing. When you short a stock, your broker lends you shares from their inventory or another client’s margin account. You immediately sell these borrowed shares at the current market price. You now have cash from the sale, but you also have an obligation to return the same number of shares to the lender.

Your goal is for the stock price to drop. If it does, you can buy back the shares at the lower price, return them to the lender, and pocket the difference. For example, if you short 100 shares at $50 per share, you receive $5,000. If the price drops to $40, you buy back the shares for $4,000, return them, and keep the $1,000 profit minus fees.

Several key terms are essential to understand. A margin account is required for short selling because you are borrowing both shares and money. The cover position refers to buying back shares to close your short. Borrow fees or short interest are the costs you pay for borrowing shares. Days to cover measures how many days it would take for all short sellers to close their positions based on average trading volume.

Short selling serves multiple purposes in markets. It provides price discovery by allowing negative opinions to be expressed through trading. It creates market efficiency by preventing overvalued stocks from becoming too inflated. It enables hedging for investors who want to protect long positions. And it provides liquidity during volatile periods.

How Does Short Selling Work?

Understanding the mechanics of short selling requires looking at each step in detail. The process involves coordination between you, your broker, and the securities lending market. Let us break down exactly how shares move from borrower to seller and back again.

First, your broker must locate shares to lend you. Not all stocks are available for shorting. Popular stocks with high trading volume are usually easy to borrow. Small-cap stocks or those with limited float may be hard to borrow, requiring you to pay higher fees or making them unavailable entirely. Your broker checks their securities lending desk or external sources to find available shares.

Once shares are located, you execute a short sale order through your broker. This is typically done by selecting “sell short” instead of “sell” in your trading platform. The broker borrows the shares on your behalf and sells them immediately at the current market price. The proceeds from this sale are credited to your account, but they are not yours to withdraw freely.

The cash from the short sale serves as collateral. Your broker holds these proceeds plus requires additional margin as security. Federal Reserve Regulation T requires at least 50% margin for short sales, though many brokers require more. This means if you short $10,000 worth of stock, you need at least $5,000 in additional margin equity in your account.

While your position remains open, you pay borrow fees daily. These fees vary widely based on demand. Easy-to-borrow stocks might cost 0.3% annually. Hard-to-borrow stocks can charge 50% or more annually. If the stock pays dividends during your short position, you must pay those dividends to the lender since they no longer hold the shares.

Here is a detailed numerical example showing both profit and loss scenarios. Suppose you short 100 shares of Company XYZ at $100 per share:

Profit Scenario:

- Sell 100 borrowed shares at $100 = $10,000 proceeds

- Stock falls to $80 per share

- Buy back 100 shares at $80 = $8,000 cost

- Gross profit = $2,000

- Less borrow fees (30 days at 5% annual on $10,000) = $41

- Net profit = $1,959

Loss Scenario:

- Sell 100 borrowed shares at $100 = $10,000 proceeds

- Stock rises to $130 per share

- Buy back 100 shares at $130 = $13,000 cost

- Gross loss = $3,000

- Plus borrow fees (60 days at 5% annual) = $82

- Net loss = $3,082

Extreme Loss Scenario (Short Squeeze):

- Sell 100 borrowed shares at $100 = $10,000 proceeds

- Stock surges to $400 per share (GameStop-style squeeze)

- Buy back 100 shares at $400 = $40,000 cost

- Gross loss = $30,000

- This is 300% of your original short value

To close your position, you execute a cover order. This buys back the same number of shares you shorted and returns them to the lender. Once covered, your obligation is eliminated and any remaining collateral is released back to your buying power.

How to Short a Stock: Step-by-Step Process

Now that you understand the mechanics, here is the practical process for executing a short trade. These five steps walk you from preparation through position closure.

Step 1: Open and Fund a Margin Account

You cannot short sell in a standard cash account. You need a margin account that allows borrowing. Apply through your broker, complete additional agreements acknowledging short selling risks, and deposit sufficient funds. Most brokers require at least $2,000 to open a margin account, though more is recommended for short selling specifically.

Step 2: Locate Shares Available to Borrow

Before attempting to short, verify the stock is available. Your broker’s platform typically shows a “shortable” indicator or borrow availability. Some brokers offer hard-to-borrow locates for a fee if standard inventory is exhausted. Large-cap stocks like Apple or Microsoft are almost always available. Small-cap biotech stocks may frequently be unavailable.

Step 3: Execute the Short Sale

Enter a sell short order through your trading platform. Specify the number of shares and order type. Many short sellers use limit orders rather than market orders to ensure they get their desired entry price. Your broker borrows shares and executes the sale. The proceeds appear in your account but are held as collateral.

Step 4: Monitor Your Position and Manage Risk

Active monitoring is essential. Watch the stock price, your account equity, and any news affecting the company. Set buy-stop orders to automatically cover your position if the price rises to a predetermined level. Monitor borrow fees, which can increase suddenly if demand spikes. Watch for dividend announcements, as you will owe those payments.

Step 5: Close Your Position (Cover)

When you are ready to exit, execute a buy-to-cover order. This purchases shares and automatically returns them to the lender. You can cover at any time, regardless of profit or loss status. You are not required to hold until a specific date. Once covered, calculate your final profit or loss after accounting for all borrow fees and dividend payments.

Pros and Cons of Short Selling

Before engaging in short selling, weigh the advantages against the significant risks. This comparison table summarizes the key points:

| Advantages | Disadvantages |

|---|---|

| Profit from declining prices | Unlimited loss potential |

| Hedge existing long positions | Margin calls can force liquidation |

| Portfolio diversification in bear markets | Borrow fees reduce profits |

| Contributes to market efficiency | Dividend payments owed to lender |

| Exposure of overvalued companies | Timing risk – markets can stay irrational |

| Liquidity provision during volatility | Regulatory restrictions can limit activity |

| Profit in any market direction | Psychological stress of betting against consensus |

| Can use technical analysis for entry | Short squeezes can cause catastrophic losses |

The primary advantage is obvious: short selling allows you to profit when markets fall. During the 2008 financial crisis or the 2020 COVID crash, short sellers generated returns while long-only investors suffered losses. Short selling also provides a hedging tool. If you own significant long positions but fear a short-term correction, shorting an index ETF can offset potential losses.

However, the disadvantages are severe and real. The unlimited loss potential is the most dangerous aspect. When you buy a stock long, your maximum loss is 100% of your investment. When you short a stock, your maximum loss is theoretically infinite because there is no ceiling on how high a stock can rise. A $50 stock can go to $500, $1,000, or higher.

Borrow fees create a time pressure that long positions do not face. Every day you hold a short position, you pay fees. If a stock remains flat for months, you accumulate costs while earning nothing. This makes short selling more expensive than long investing for positions held over extended periods.

Understanding the Risks of Short Selling

Short selling is one of the highest-risk strategies available to retail investors. Understanding these risks completely is essential before attempting your first short trade. Here are the major dangers you face.

Unlimited Loss Potential

This is the risk that terrifies experienced traders. When you buy a stock at $50, the worst case is the company goes bankrupt and the stock goes to zero. You lose your $50 per share. When you short a stock at $50, the worst case is theoretically unlimited. The stock could rise to $100, $500, or $1,000. You are obligated to buy it back at whatever price it reaches.

Consider the GameStop short squeeze of 2021. hedge funds had shorted GameStop at prices between $10 and $50. When retail investors organized buying campaigns, the stock rose above $480 per share. Short sellers faced losses of 900% or more. Several hedge funds went bankrupt. Individual traders lost life savings.

Margin Calls

Your broker requires collateral for short positions. If the stock price rises, your account equity decreases. When equity falls below maintenance margin requirements (typically 30-35%), you receive a margin call. You must either deposit more funds or your broker will forcibly close your position by buying back shares at the current market price.

Margin calls can occur with devastating speed. A stock that gaps up 30% overnight on unexpected news can trigger immediate margin calls. You might not have time to react before your broker closes your position, locking in losses. This forced liquidation is one of the most painful aspects of short selling.

Short Squeeze Risk

A short squeeze occurs when heavily shorted stocks experience rapid price increases, forcing short sellers to buy back shares to cover losses. This buying pressure drives prices even higher, creating a feedback loop. Stocks with high short interest relative to their float are most susceptible to squeezes.

Beyond GameStop, other notable squeezes include Volkswagen in 2008, which briefly became the world’s most valuable company as short sellers scrambled to cover. More recently, various meme stocks have experienced violent squeezes. Always check a stock’s days-to-cover ratio before shorting. Anything above 5 days indicates elevated squeeze risk.

Dividend and Corporate Action Obligations

When you short a stock that pays dividends, you must pay those dividends to the lender. If a $100 stock pays a $2 quarterly dividend, you owe $2 per share while holding the short position. This further erodes your returns. You also face obligations during stock splits, spin-offs, and mergers, which can complicate your position.

Borrow Fee Increases

Borrow fees are not fixed. They fluctuate based on supply and demand. A stock that cost 2% annually to borrow might spike to 100% or more if short interest suddenly increases. During the GameStop saga, borrow fees exceeded 200% for some periods. These fees accumulate daily and can turn a profitable short into a losing trade even if the stock price declines.

Regulatory and Exchange Restrictions

During periods of extreme volatility, regulators may impose short selling restrictions. The SEC can ban short selling in specific stocks or entire markets. Exchanges may increase margin requirements suddenly. These interventions can trap short sellers, preventing them from exiting positions or requiring additional capital they do not have.

What Is a Short Squeeze?

A short squeeze is a rapid increase in a stock’s price that forces short sellers to buy back shares to close their positions, which in turn drives the price even higher. This creates a vicious cycle where buying begets more buying, often sending prices far beyond fundamental valuations.

Squeezes typically occur in stocks with high short interest relative to their trading volume. When days to cover exceeds 5 or 10, it indicates that closing all short positions would take significant time. This creates a powder keg situation. Any positive catalyst, whether earnings, news, or coordinated buying, can ignite the squeeze.

The GameStop saga of January 2021 remains the most famous modern example. GameStop had short interest exceeding 100% of its float at times, meaning more shares were sold short than actually existed in the market. When retail traders from Reddit’s WallStreetBets forum began buying shares and call options en masse, the price rose from under $20 to over $480 in weeks.

Short sellers faced impossible choices. Covering would lock in massive losses. Not covering meant facing margin calls and potentially unlimited further losses. hedge funds like Melvin Capital lost billions and eventually closed. Individual traders lost everything when the volatility swung both directions.

To identify squeeze risk before shorting, check these metrics:

- Short interest ratio: Percentage of float sold short. Above 20% is elevated risk.

- Days to cover: Short interest divided by average daily volume. Above 5 days indicates squeeze potential.

- Hard to borrow status: If shares are scarce, a squeeze is more likely.

- Social media sentiment: Stocks trending on Reddit or Twitter carry elevated squeeze risk.

Who Engages in Short Selling?

Short selling attracts different types of market participants, each with unique motivations and strategies. Understanding who shorts and why helps contextualize this practice.

Hedge Funds

hedge funds are the most prominent short sellers. Many hedge funds employ long/short equity strategies, buying undervalued stocks while shorting overvalued ones. This market-neutral approach aims to profit from stock selection rather than market direction. Other hedge funds specialize in activist short selling, researching and publicly exposing companies they believe are fraudulent or overvalued.

Activist Short Sellers

Firms like Muddy Waters Research, Hindenburg Research, and Citron Research have built reputations by publishing detailed reports exposing corporate misconduct. These activists short a stock, publish their research, and profit if the price falls. Their reports have uncovered major frauds, including the Luckin Coffee scandal and numerous Chinese reverse-merger frauds. Critics argue they sometimes manipulate markets, while supporters credit them with improving market integrity.

Institutional Investors

Pension funds, mutual funds, and insurance companies sometimes use short selling for hedging. If a fund holds significant long positions but fears a market correction, they might short index futures or specific sector ETFs to offset risk. This is defensive short selling rather than speculative.

Day Traders and Retail Investors

Individual traders short sell for quick profits during intraday volatility. They rely on technical analysis, momentum, and news catalysts. The rise of zero-commission trading has made short selling more accessible to retail investors, though it remains risky for inexperienced traders. Many retail brokers now offer easy-to-use short selling interfaces, though they restrict access to certain hard-to-borrow stocks.

Market Makers

Market makers short sell as part of their obligation to provide liquidity. When investors want to buy shares that are not immediately available, market makers may short sell to complete the transaction, then locate shares afterward. This facilitates smooth market functioning.

Short Selling Regulations and Rules

Short selling operates within a complex regulatory framework designed to prevent market manipulation and excessive speculation. Understanding these rules is essential for compliance and risk management.

The Securities and Exchange Commission (SEC) oversees short selling in the United States. Regulation SHO, implemented in 2005, established the modern short selling framework. Key provisions include the locate requirement, which mandates that brokers must locate shares available for borrowing before executing a short sale. This prevents naked short selling, where traders sell shares without actually borrowing them first.

Naked short selling is illegal in most circumstances. It creates failure to deliver situations where shares sold do not exist. While legitimate market making activities have exemptions, naked shorting by speculators is prohibited. The SEC maintains a threshold securities list tracking stocks with elevated fail-to-deliver rates.

The uptick rule, originally implemented after the 1929 crash, restricted short selling to price increases. The 2010 alternative uptick rule triggers circuit breakers when stocks drop 10% in a day, limiting short selling for the remainder of that day and the next. These restrictions aim to prevent short selling from accelerating market crashes.

Brokers must provide daily reports of short positions for regulatory surveillance. Large short positions may require disclosure to the SEC. International markets have varying rules, with some countries banning short selling entirely during crisis periods.

Account-level restrictions also apply. You cannot short sell in retirement accounts like IRAs or 401(k)s. Pattern day trader rules apply to short selling activity. And brokers reserve the right to force-close positions or increase margin requirements at any time.

Tax Implications of Short Selling

Tax treatment of short selling differs significantly from traditional long positions, and these differences can substantially impact your after-tax returns. Most educational guides ignore this critical aspect, but understanding tax implications is essential for any serious short seller.

Short selling gains are always treated as short-term capital gains, regardless of how long you hold the position. While long positions held over one year qualify for favorable long-term capital gains rates (0%, 15%, or 20%), short selling profits are taxed at ordinary income rates. This can mean paying 37% federal tax on short selling profits versus 20% on long-term gains. For high-income traders, this differential significantly reduces net returns.

Losses from short selling follow standard capital loss rules. You can deduct losses against gains, with excess losses deductible up to $3,000 annually against ordinary income. However, wash sale rules complicate short selling strategies. If you close a short position at a loss and enter a new short position in the same or substantially identical security within 30 days, the wash sale rule defers the loss deduction.

Dividend payments you make while holding short positions receive particularly unfavorable treatment. When you pay dividends to the lender of borrowed shares, these payments are not deductible as investment expenses. Instead, they effectively increase your cost basis. However, if you hold the short position for 45 days or less around the dividend record date, special rules may apply that limit your ability to deduct related expenses.

Short selling in tax-advantaged accounts like IRAs is prohibited entirely. You cannot use margin in these accounts, making short selling impossible. This restriction forces traders seeking short exposure to use taxable accounts exclusively, eliminating tax deferral benefits available to long-term investors.

Reporting requirements for short selling are complex. You must track borrow fees, dividend payments, and closing dates carefully. Many traders use specialized tax software or professional preparers to ensure accurate reporting. The IRS pays particular attention to short selling on audits due to potential for tax avoidance schemes.

Consider this tax comparison: A trader earns $10,000 short selling Stock A held for 6 months and $10,000 buying and holding Stock B for over one year. The short selling profit might incur $3,700 in federal taxes at the 37% rate. The long-term gain incurs only $2,000 at the 20% rate. The tax drag on short selling is nearly double.

Alternatives to Short Selling

Given the unlimited loss potential, borrowing costs, and unfavorable tax treatment of short selling, many investors prefer alternative strategies for profiting from declining prices. These alternatives often provide better risk management and tax efficiency.

Put Options

Buying put options is the most popular short selling alternative. A put option gives you the right to sell a stock at a predetermined price (the strike price) until a specific expiration date. Your maximum loss is limited to the premium paid for the option, unlike short selling’s unlimited risk. If the stock drops below the strike price minus the premium, you profit.

Options also offer leverage. Controlling 100 shares with a put option costs significantly less than the margin required to short 100 shares. However, options expire worthless if the stock does not move in your favor by expiration, creating time pressure that short selling does not have.

Inverse ETFs

Inverse exchange-traded funds aim to deliver the opposite of their underlying index’s daily performance. ProShares Short S&P 500 (SH) seeks daily investment results that correspond to the inverse of the S&P 500’s daily performance. These ETFs trade like stocks, require no margin account for basic purchases, and have defined loss limits.

However, inverse ETFs suffer from volatility decay in choppy markets. Because they rebalance daily to maintain inverse exposure, sideways markets erode value over time. They are best suited for short-term trades during clear directional moves rather than long-term hedges.

Bear Market Mutual Funds

Some mutual funds specialize in short selling or holding inverse index positions. These provide professional management for investors who want short exposure without executing trades themselves. Rydex and ProFunds offer various bear market funds targeting different indices. Expense ratios are higher than standard index funds but lower than the borrow fees you might pay shorting directly.

Covered Calls on Existing Positions

If you want downside protection rather than pure short speculation, selling covered calls on your long positions generates income that offsets potential losses. This is not a true short alternative but rather a hedging strategy. The income from call premiums reduces your net cost basis, providing a small cushion against price declines.

Comparison Summary

Put options offer the best risk-limited alternative for betting on specific stock declines. Inverse ETFs work well for broad market downside bets without stock-specific research. Short selling itself remains most appropriate for sophisticated traders seeking maximum leverage and precision in their downside bets, assuming they can manage the risks.

Frequently Asked Questions

Do you make money shorting if the price goes down?

Yes, you profit when shorting if the stock price declines. When you short sell, you borrow and sell shares at the current price, then buy them back later at a lower price to return to the lender. The difference between your higher sale price and lower repurchase price equals your gross profit, minus any borrowing fees and dividends paid during the holding period.

How to make profit when stock goes down?

To profit from a declining stock, open a margin account with a broker, locate shares available to borrow, execute a short sale at the current price, wait for the stock to fall, then buy back the shares at the lower price to cover your position. The profit equals the price difference minus fees. Alternatively, buy put options or inverse ETFs which offer limited risk compared to direct short selling.

How do short sellers make a stock go down?

Short sellers themselves do not directly make stocks decline, though heavy short selling can create selling pressure. Activist short sellers may publish negative research about companies, which can cause selling if the research convinces other investors. However, short sellers cannot force prices down artificially without violating market manipulation laws. Ultimately, stock prices reflect fundamental value, market sentiment, and broad economic forces beyond any single participant’s control.

What is the 3-5-7 rule in trading?

The 3-5-7 rule in trading refers to a risk management framework for position sizing and loss limits. Traders risk no more than 3% of their portfolio on a single trade, cut losses at 5% decline from entry, and avoid holding positions showing 7% or greater losses. While not specific to short selling, this rule helps short sellers manage the unlimited loss potential inherent in their strategy by enforcing strict stop-loss discipline.

Is short selling illegal?

Short selling is legal in the United States and most developed markets when conducted properly. Illegal activities include naked short selling (selling shares without borrowing them first), spreading false information to manipulate prices, and coordinated bear raids intended to destroy legitimate companies. The SEC regulates short selling through Regulation SHO, which mandates locate requirements and prevents failures to deliver. Some countries ban short selling during financial crises.

Can you lose more than you invest short selling?

Yes, you can lose far more than your initial investment when short selling. Unlike buying stocks long, where maximum loss is 100% of your investment, short selling has theoretically unlimited loss potential. A stock you short at $50 can rise to $500 or higher, meaning you could lose 1000% or more of your original position value. This is why risk management, stop-loss orders, and position sizing are absolutely critical for short sellers.

How much money do you need to start short selling?

Most brokers require at least $2,000 to open a margin account, which is the minimum for short selling. However, experienced traders recommend having $25,000 or more to avoid pattern day trader restrictions and to maintain adequate margin cushions. Short selling requires additional capital beyond the position value because you must maintain margin requirements, and brokers may increase these requirements suddenly during volatile periods.

How long can you hold a short position?

There is no time limit on how long you can hold a short position, provided you maintain adequate margin and the shares remain available to borrow. However, holding short positions indefinitely is expensive due to daily borrow fees that accumulate over time. Additionally, brokers can recall borrowed shares at any time, forcing you to cover your position. Most short sellers aim for quick profits rather than long-term short holds.

Final Thoughts

Short selling remains one of the most powerful yet dangerous tools in an investor’s arsenal. It offers the unique ability to profit from declining prices, hedge existing portfolios, and contribute to market efficiency by exposing overvalued securities. For sophisticated traders who understand the mechanics and manage risks effectively, short selling can generate returns in any market environment.

However, the risks cannot be overstated. Unlimited loss potential, margin call exposure, short squeeze dangers, and unfavorable tax treatment make short selling inappropriate for most retail investors. Our analysis shows that the majority of individual traders who attempt short selling without proper education and risk management suffer significant losses.

If you are determined to explore short selling, start small. Use strictly limited position sizes. Always employ stop-loss orders. Never short stocks with high days-to-cover ratios or significant short squeeze potential. Consider alternatives like put options that offer defined risk limits. And never short with capital you cannot afford to lose entirely.

For most investors, the safer path involves building diversified long-term portfolios, using inverse ETFs for occasional hedging, and leaving aggressive short selling to professionals with the capital, experience, and risk tolerance to handle its unique challenges. Sometimes the smartest trade is the one you do not make.